Are payroll taxes deducted from Social Security?

Social Security is financed through a dedicated payroll tax. In 2019, $944.5 billion (89 percent) of total Old-Age and Survivors Insurance and Disability Insurance income came from payroll taxes.

What type of taxes do employers withhold from your paycheck?

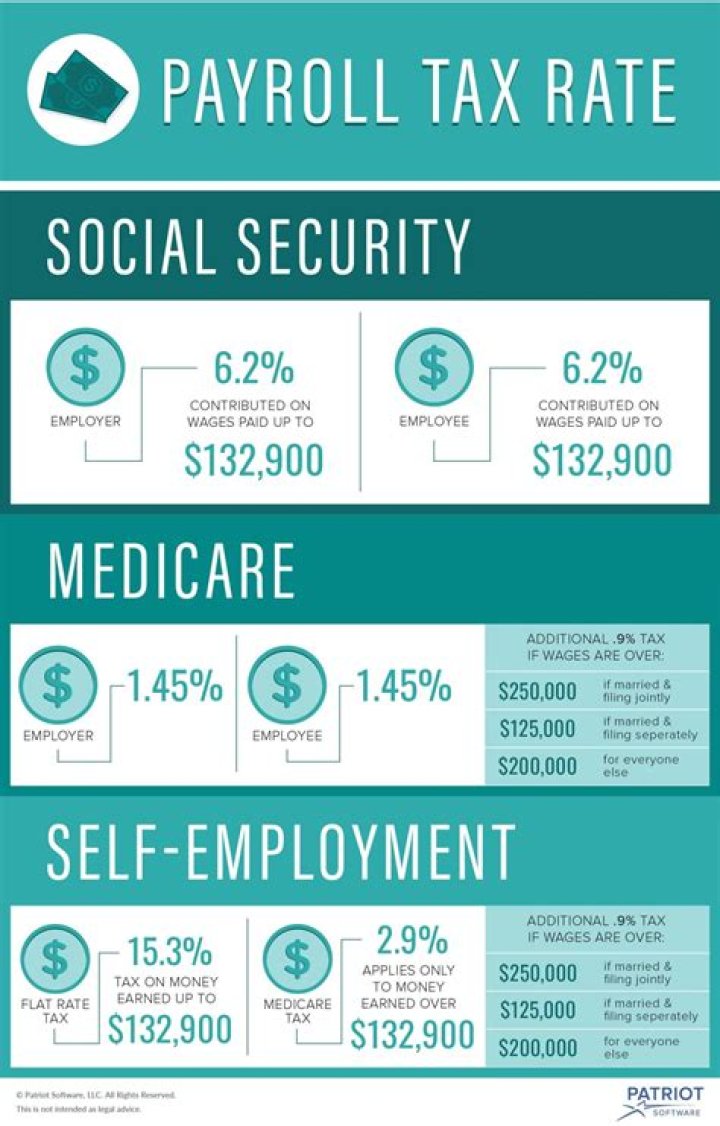

That’s because the IRS imposes a 12.4% Social Security tax and a 2.9% Medicare tax on net earnings. Typically, employees and their employers split that bill, which is why employees have 6.2% and 1.45%, respectively, held from their paychecks.

Is payroll tax the same as Social Security withholding?

Payroll tax consists of Social Security and Medicare taxes, otherwise known as Federal Insurance Contributions Act (FICA) tax. FICA tax is an employer-employee tax, meaning both you and your employees contribute to it. Payroll tax is a percentage of an employee’s pay.

How much tax is withheld from an employee’s paycheck?

The calculation for these deductions is pretty straightforward. The amount of FICA tax is 15.3% of the employee’s gross pay. Half of the total (7.65%) is withheld from the employee’s paycheck, and half is paid by the employer.

Do you have to pay Social Security tax as an employer?

Every employee and employer in the U.S. is required to pay Social Security tax. As an employer, you will withhold the tax from employee wages. You will also make a Social Security contribution based on the employee’s wages. Social Security tax is one part of FICA tax. The other part of FICA tax is Medicare tax.

What happens when employer does not withhold Social Security?

As an employee, your employer must deduct Social Security and other state, local and federal taxes mandated under statute. If you are classified as an employee and your employer does not withhold Social Security tax, file a case with the IRS.

Can a employer withhold taxes from a paycheck in California?

In California, it is not recommended that employers withhold unpaid taxes from an employee’s final paycheck, even with a signed agreement. If necessary, an employer can make a separate arrangement to collect the total applicable taxes from the former employee; otherwise, the employer would have to pay the balance owed.