Are section 1231 losses deductible?

Understanding Section 1231 Property However, when losses are recorded on section 1231 property whereby the loss is classified as an ordinary loss, it’s 100% deductible against their income.

Where does Section 1231 loss get reported?

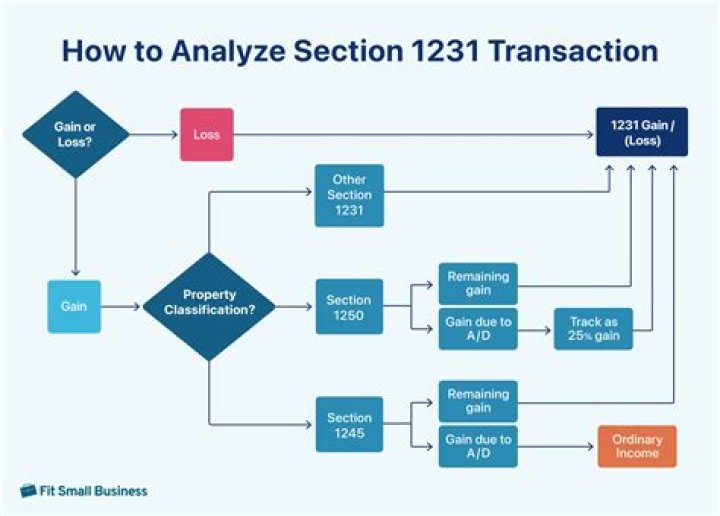

Section 1231 losses are treated as ordinary losses and reduce other ordinary income (such as wages). Section 1231 gains are given long term capital gain treatment and subsequently reported on Schedule D.

Do section 1231 losses expire?

If capital losses exceed capital gains in any given tax year, the excess loss may be carried back three years and carried forward five years where it is offset against capital gains of those years. Section 1231 does not reclassify property as a capital asset.

Is the section 1231 loss reported as ordinary income?

The amount of the loss that is applied against the current year’s section 1231 gain is reported as ordinary income. The balance of the current year’s section 1231 gain that exceeds the recaptured section 1231 loss from the previous five years is reported as long-term capital gain.

How are long term capital gains treated under Section 1231?

the section 1231 losses for such taxable year, such gains and losses shall be treated as long-term capital gains or long-term capital losses, as the case may be. such gains and losses shall not be treated as gains and losses from sales or exchanges of capital assets. Such term does not include poultry.

How to recapture nonrecaptured net section 1231 losses?

How to Recapture Nonrecaptured Net Section 1231 Losses. The Purpose of the Loss Recapture Rule. The reason nonrecaptured section 1231 losses must be recaptured over a five-year period is to prevent gain and loss manipulation from year to year.

Why is Section 1245 referred to as Section 1231?

Section 1245 property that is held more than one year at the time of disposal is also referred to as Section 1231 property because the tax rules of Section 1231 apply when such property is disposed of. $7,000. Less: Recaptured depreciation. Note: Recaptured depreciation is reported as ordinary income.