Can a short term capital loss be set off against a long term capital gain?

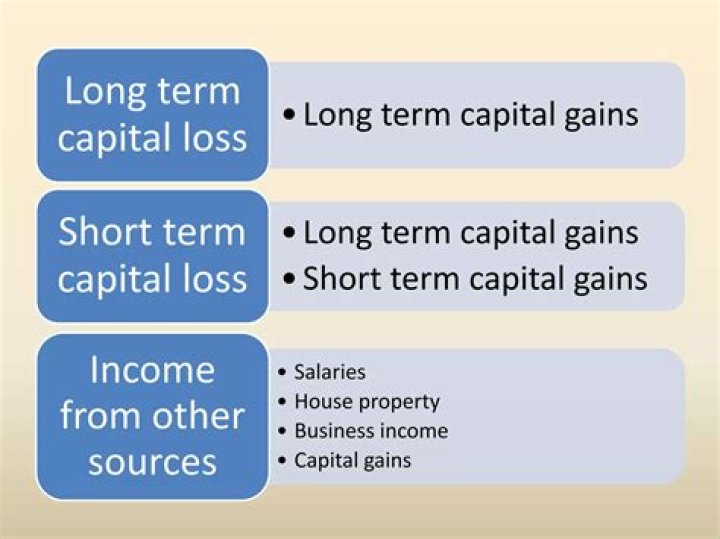

2) Long-term capital loss cannot be set off against any income other than income from long-term capital gain. However, short-term capital loss can be set off against long-term or short-term capital gain.

How are short term losses used to offset regular income?

The amount of the short-term loss is the difference between the basis of the capital asset–or the purchase price–and the sale price received for selling it. Short-term losses can be used to offset short-term gains that are taxed at regular income, which can range from 10% to as high as 37%. Breaking Down Short-Term Loss

How much is a short-term unrealized loss allowed?

A short-term unrealized loss describes a position that is currently held at a net loss to the purchase price but has not been closed out (inside of the one-year threshold). Net short-term losses are limited to a maximum deduction of $3,000 per year, which can be used against earned or other ordinary income. 1

Can a capital loss be carried forward to the next year?

If loss under the head “Capital gains” incurred during a year cannot be adjusted in the same year, then unadjusted capital loss can be carried forward to next year.

Short-term capital losses can be set off against short-term as well as long-term capital gains. Quick Tip: Long-term capital losses can be carried forward to a maximum of 8 years and set off against long-term capital gains. Capital gains can broadly be classified into two types:

What was long term capital gain under Income Tax Act 1961?

The Article Discusses about Tax Treatment of Long Term Capital Gain arising from Transfer of Capial Assets under Income Tax Act, 1961.

What is gain or loss from trading of Section 1256 Contracts?

For purposes of this title, gain or loss from trading of section 1256 contracts shall be treated as gain or loss from the sale or exchange of a capital asset.

Which is used to calculate long term capital gains?

For calculating capital gains on long-term assets, indexation is used. CII or Cost Inflation Index is used in the computation of long-term capital gains tax. The CII is notified through a notification issued by the Income Tax Department each financial year.