Can an LLC be cash basis?

Accounting Methods for an LLC One can choose to use either the accrual basis or cash basis of accounting when initially setting up the accounting system for an LLC. Under the cash basis, revenue is recognized when cash is received and expenses when bills are paid.

How do you do bookkeeping for rental property?

Rental Property Bookkeeping 101

- Separate your personal and business accounts.

- Set up individual accounts for each property.

- Implement a system for tracking your income and expenses.

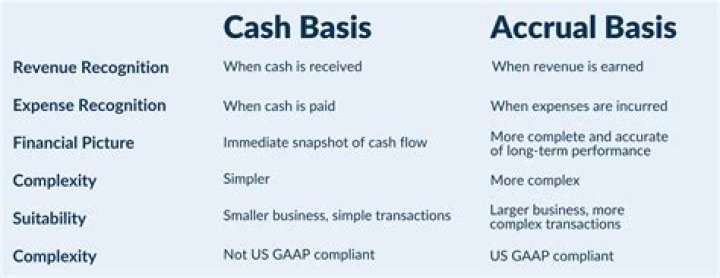

- Choose between the cash or accrual accounting methods.

- Take advantage of accounting technology.

- Prepare for fluctuating expenditures.

Is rental income accrual or cash basis?

When to Report Income Report rental income on your return for the year you actually or constructively receive it, if you are a cash basis taxpayer. You are a cash basis taxpayer if you report income in the year you receive it, regardless of when it was earned.

Is rental income on a cash basis?

With effect from 6 April 2017 (individual) landlords are now required to report their rental income and expenditure on a cash basis. From 6 April 2017 the cash basis must be used unless: The property business is carried on by a company, an LLP, a partnership with a corporate member or a trust.

How is rental income accounted for?

To account for rent income you have earned but will collect at a later date, debit the rent receivable account by the portion earned, and credit the rent income account by the same amount. The debit increases the receivables account, which is an asset that shows money your tenant owes.

How is rental income calculated on a cash basis?

Rental Income on Cash Basis. Landlords of unincorporated properties can make use of the simplified accounting process to calculate taxable profits. This will not only take the tax returns process into the digital age, it will also cut down on the need for adjustment, which was necessary in the traditional accounting process.

Are there any restrictions on cash basis for landlords?

HMRC’s specific guidance on the cash basis for landlords can be found at PIM1090 onwards. Loan interest – there are additional restrictions further to those which relate to other residential property businesses since 6 April 2017 (see PIM1094 ). The normal £500 restriction to finance charges for cash accounting does not apply

When to use cash basis for letting business?

It applies for unincorporated letting businesses with gross rents of less than £150,000. The statutory default position is the cash basis, but an election can instead be made to prepare the rental accounts under GAAP accounting It applies to both commercial and residential letting businesses.

How does cash basis work for unincorporated properties?

Cash basis which was once limited to only a few types of businesses have now been extended to unincorporated properties. Here is a look at how cash basis will work for landlords of unincorporated properties.