Can depreciation policy be changed?

At the end of each financial year, management should review the method of depreciation. Thus, the method of depreciation can be changed without retrospective effect or with retrospective effect.

What GAAP applies to depreciation?

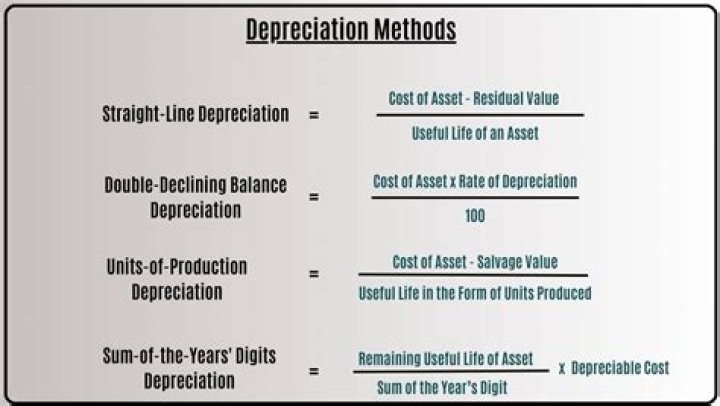

Accountants must adhere to generally accepted accounting principles (GAAP) for depreciation. There are four methods for depreciation allowable under GAAP, including straight line, declining balance, sum-of-the-years’ digits, and units of production.

Is a change in depreciation a change in accounting policy?

On the same footings, change in depreciation method is not a change in accounting policy rather it is a change in accounting estimate. Change in accounting policy only occurs if rules of either recognition, measurement or presentation of line item are changed. Therefore, it is a change in accounting estimate.

Does GAAP require straight line depreciation?

The straight line method of depreciation is the simplest method of depreciation. Using this method, the cost of a tangible asset is expensed by equal amounts each period over its useful life. The idea is that the value of the assets declines at a constant rate over its useful life. This method is approved by GAAP.

What is the least used depreciation method in GAAP?

Straight line depreciation

Straight line depreciation is often chosen by default because it is the simplest depreciation method to apply. You take the asset’s cost, subtract its expected salvage value, divide by the number of years it’s expect to last, and deduct the same amount in each year.

What are the different methods of depreciation under GAAP?

There are four different methods for depreciating assets under GAAP: straight line method, units of production method, declining balance method and the sum of years. Different rules apply depending on which method you use.

When do you have to change the depreciation method?

Due to this requirement, if the consumption pattern of economic benefits changes then entity might have to change the depreciation method. Change in depreciation method is a change in accounting estimate and NOT a change in accounting policy.

How do you correct a depreciation accounting error?

Depreciation errors are corrected by either filing an amended return or filing a change in accounting method form. Depreciation errors that are NOT subject to the accounting method change filing requirements require amended returns and include: You claimed the incorrect amount because of a mathematical error made in any year.

How many years does it take to depreciate an asset?

The depreciation estimate journal each year would be as follows: As time passes, the asset is depreciated at this rate and after 4 years the accumulated depreciation on the asset is 12,000 x 4 = 48,000.