Can dividend income be set off against capital losses?

To address this, section 94 (7) of the Income-Tax Act was introduced. In such cases, the capital loss arising to the shareholder to the extent of such dividend income shall be ignored i.e. the loss would not be available for set off against capital gain income. Example: Mr A bought 1000 shares of B Co.

What can non-capital losses be applied against?

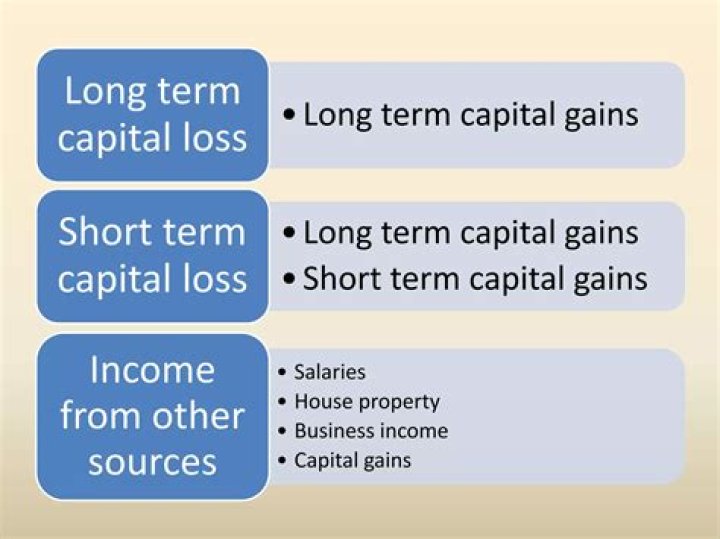

Non-capital losses generally include losses from a business or employment. These losses can be applied to reduce all sources of income in the current tax year, the previous 3 years and the next 20 years. These losses can only be applied against taxable capital gains in the current tax year or subsequent years.

How is non capital loss applied in taxes?

How is non-capital loss applied? Unlike capital losses, non-capital losses can be applied to other income. If your small business venture resulted in a loss of $5000, that loss can be applied to the income from your other sources such as employment, RRSP income, interest amounts, etc.

Can a capital loss be used to offset dividends?

Although dividends and long-term capital gains are taxed at the same rates, this does not mean that capital losses can be used to offset dividends. However, if you have a net capital loss after offsetting all capital gains, up to $3,000 per year of capital loss may offset regular taxable income which may include dividends.

Can a capital loss wipe out qualified dividend income?

Therefore, the loss would decrease the amount of taxable capital gain income. If you had $1000 of qualified dividends, then a long-term capital loss of $1000 or more (up to the $3,000 capital loss cap for married filing jointly) would wipe out the qualified dividend income.

Do you have to claim capital gains on dividends?

Offsetting Dividend Income. Investors only need to claim capital gains and losses when they sell stock. However, they must claim dividends each year they receive them. One way to offset dividend income directly and consistently is by itemizing your deductions and claiming your investment expenses.