Can I open an IRA in 2021 for 2020 taxes?

You can contribute to an IRA at any time during the calendar year and up to tax day of the following calendar year. For example, taxpayers can contribute at any time during 2020 and have until the tax deadline (May 17, 2021) to contribute to an IRA for the 2020 tax year.

Should I fund my IRA at the beginning of the year?

Her verdict: The best time to fund an IRA is January 1st of the tax year. If the money is sitting in an interest bearing taxable account, you will lose some of the earnings to taxes. If instead, you put the money into an interest-bearing, IRA it will earn the same interest tax-deferred.

Is now a good time to invest in IRA?

If you can manage it, it’s also a great time to make both your 2020 and 2021 contributions. You are eligible to contribute up to $6,000 for each year — meaning a $12,000 contribution to invest and grow tax-free forever if you deposited both today.

Can you invest more than you earn in a year in an IRA?

You can’t contribute more than you earned in a particular year, even if you have the money in other savings. Once the money is in the account, you can invest it in whatever is offered through the account, including stocks, bonds, mutual funds and other typical investments.

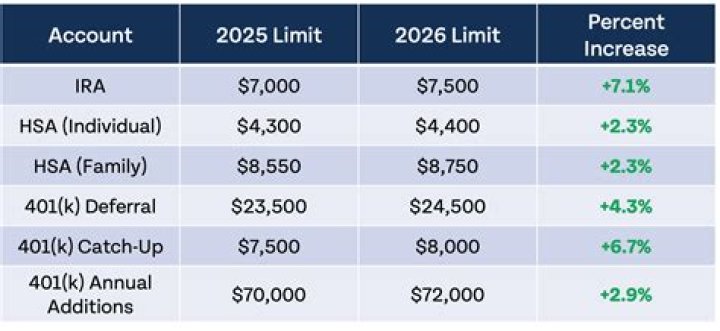

What’s the maximum contribution to an IRA per year?

IRAs in 2021 are unchanged from 2020 (and 2019): they have an individual contribution limit of $6,000, with an additional $1,000 allowed for earners 50+ years old. A non-working spouse can also contribute up to $6,000. These limits presume you, or you are your spouse, are reporting earned income on your tax return.

How much can I save on taxes with an IRA?

How much you can save on taxes with an IRA depends on your tax brackets when you make deductible IRA contributions and make withdrawals, as well as how much you put into the account. If you withdraw money early from your IRA, you may owe a tax penalty that can limit your total earnings or even effectively erase those IRA tax benefits.

How old do you have to be to take money out of an IRA?

To take advantage of this tax-free withdrawal, the money must have been deposited in the IRA and held for at least five years and you must be at least 59½ years old. If you need the money before that time, you can take out your contributions with no tax penalty so long as you don’t touch any of the investment gains.