Can I rollover after-tax contributions to a traditional IRA?

This means you can roll over all your pretax amounts to a traditional IRA or retirement plan and all your after-tax amounts to a different destination, such as a Roth IRA. A distribution of $10,000 in after-tax amounts to yourself.

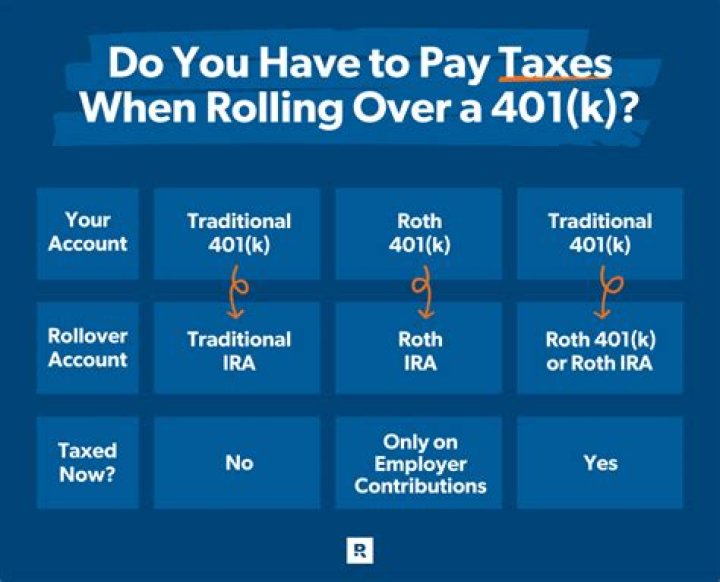

Is Rollover IRA a traditional IRA?

A rollover IRA can be a traditional IRA. It can also be a Roth IRA if you want to roll money from a Roth 401(k).

Can traditional IRA be pre taxed?

A Traditional IRA is an Individual Retirement Account to which you can contribute pre-tax or after-tax dollars, giving you immediate tax benefits if your contributions are tax-deductible. Unlike with a Roth IRA, there are no income limitations to open a Traditional IRA.

Can I contribute to a traditional IRA with post tax dollars?

In addition to non-taxable contributions to a Traditional IRA (TIRA) – discussed in a previous article – investors can contribute additional after-tax funds to their TIRAs, which can not be deducted from one’s federal tax liability.

Is a rollover IRA different from a traditional IRA to another IRA must be done within?

(To avoid tax consequences, a rollover from a Traditional IRA to another IRA must be done within 60 days.) ( A defined contribution plan is considered a tax-qualified plan.)

What should I do with my rollover IRA?

A Rollover IRA is an account that allows you to move funds from your old employer-sponsored retirement plan into an IRA. With an IRA rollover, you can preserve the tax-deferred status of your retirement assets, without paying current taxes or early withdrawal penalties at the time of transfer.

How does a rollover from a pre-tax retirement plan work?

The easiest transfer for a pre-tax retirement plan is a rollover into another pre-tax plan. This is usually a transfer into another company’s 401 (k) or into a traditional IRA.

When do I have to pay taxes on a direct rollover?

However, they must complete the process within 60 days to avoid income taxes on the withdrawal. If they miss the 60-day deadline, the IRS treats the amount like an early distribution. Direct rollover assets are made payable to the qualified plan or IRA custodian or trustee and not to the individual.

How are rollover IRAs reported to the IRS?

IRA rollovers are reported on tax returns as non-taxable transactions. As per the IRS: ” If you’re getting a distribution from a retirement plan, you can ask your plan administrator to make the payment directly to another retirement plan or to an IRA.”

What is a direct rollover from an IRA to a 403B?

It can also be a distribution from an IRA to a qualified plan, 403 (b) plan or a governmental 457 plan. A direct rollover effectively allows a retirement saver to transfer funds from one retirement account to another without penalty and without creating a taxable event.