Can LLC be accrual basis?

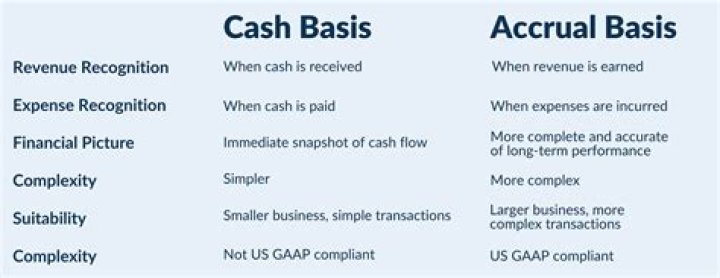

Accounting Methods for an LLC One can choose to use either the accrual basis or cash basis of accounting when initially setting up the accounting system for an LLC. Under the accrual basis, revenue is recognized when earned and expenses when incurred.

Can an individual be an accrual basis taxpayer?

Most individual taxpayers are cash basis taxpayers. Taxpayers on a cash basis may choose to use the accrual method to determine the foreign tax credit. However, once this choice has been made, the taxpayer must use the accrual method for the foreign tax credit on all future tax returns.

Who must be an accrual basis taxpayer?

The accrual method is required if the entity fails both the $1 million and the material income-producing factor tests. The accrual method is required if the company has more than $5 million in average sales. The exhibit below includes a flow chart to help small businesses select the proper accounting method.

Can a partnership be accrual basis?

Generally, a small business can use either the overall cash method of accounting or an overall accrual method of accounting. C corporations and partnerships with a C corporation as a partner can use the cash method if their average annual gross receipts for the prior three tax years are less than $5 million.

When do you use accrual basis in accounting?

Accrual-basis accounting helps you record your business activity as it happens, even if cash has not yet changed hands. Most businesses use this method rather than cash-basis accounting.

Do you have to report income on an accrual basis?

However, it involves special rules, and income and expenses need to use the same reporting method, whether you choose cash or accrual. In other words, you cannot record your income using the cash method and record expenses with the accrual method. It’s best to get advice from a tax accountant if you fall into this category.

Can you deduct LLC losses on an outside basis?

If a member is allocated both income and deductions for a tax year in which he or she has a net LLC loss in excess of his or her outside basis, the member can deduct LLC losses up to the amount of allocated LLC income. Presumably, the member deducts a pro rata portion of each separately stated loss item up to the amount of allocated income.

Can a partnership be on the accrual method?

Also, the accrual method can be mandated by the IRS if it more accurately reflects income than does the cash method.