Can long-term care premiums increase?

According to the American Association for Long-Term Care Insurance, premiums are increasing due to lapse rates, longer lives, increased cost of care, and interest rates. Insurance companies are required to keep so much cash in reserves to pay out future claims.

How often do long-term care premiums increase?

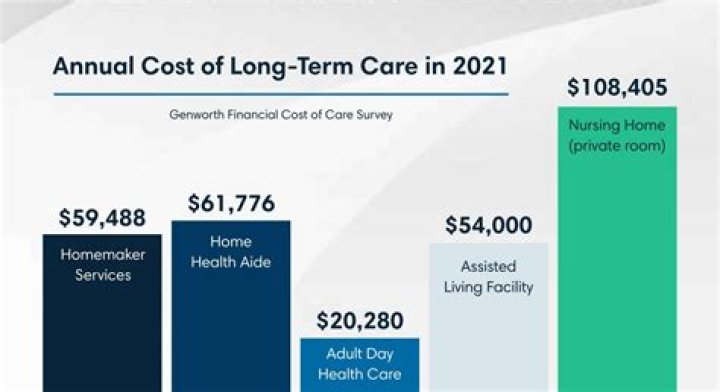

HOW MUCH DOES LONG-TERM CARE COST? The cost of care in the future will be much higher than it is today. California nursing home rates increased at an average rate of over 5% per year during the past twenty years and are likely in the future to continue to increase by at least 5% per year.

What would decrease the premium for a long-term care policy?

A lower daily benefit will mean lower premiums. Inflation protection. If you are purchasing a long-term care policy and are younger than age 62 or 63, you will need to purchase compound inflation protection. This can, however, more than double your premium.

What is a benefit increase option in long term care insurance?

The benefit increase option allows you to increase your daily benefit amount, monthly maximums and total coverage amount on a periodic basis. You can purchase additional coverage without having to provide proof of insurability.

What are long-term care premiums?

Long-term care insurance (LTC or LTCI) is an insurance product, sold in the United States, United Kingdom and Canada that helps pay for the costs associated with long-term care. Long-term care insurance covers care generally not covered by health insurance, Medicare, or Medicaid.

How old is the typical purchaser of long-term care insurance?

58 is the average age of purchaser (individual long-term care insurance policy). 14.3% of purcyhasers were under age 50. 46.0% were between 50 and 60.

Are payments from long-term care insurance taxable?

In general, the income from a long-term care insurance policy is non-taxable, and the premiums paid to buy the insurance are tax deductible.

What happens if you don’t use long-term care insurance?

Pro: You get something for your money even if you never use the long-term care portion of the policy. If you don’t use it for long-term care, or don’t use all of it, your beneficiary gets a life insurance payout when you die. Con: It’s an option only if you have a large sum of money to spend.

Are there long-term care insurance rate increases?

Long-term care insurers have been imposing significant rate increases for nearly a decade, and the problem has the attention of the regulators in each state, who must approve premium increases.

Which is best long term care or life insurance?

Hybrid long-term care policies combine two coverages under one policy, usually a life insurance policy or a qualifying annuity with a long-term care rider. The advantages of a hybrid life/long-term care insurance policy include: The policy will pay out a guaranteed death benefit if the policyholder doesn’t use long-term care insurance.

How does investment return affect long term care insurance?

Investment return is a critical part of pricing a long-term care insurance policy. BUT, let’s get back to long-term care insurance rate increases. First, it is important to know that each year long-term care insurers pay more claims than the year before.

How much does long term care cost per day?

Bill’s long term care costs in 2017 are $375 per day, all of which are reimbursed under his qualified long-term care insurance policy. Since the per diem amount for tax-free long-term care insurance benefits in 2017, is $360, how much of his daily benefit will he receive tax-free? B– $375