Can loss from income from other sources be carried forward?

Other loss from “income from other sources” can be set off against any other income during a financial year. However, loss from “Income from other sources” cannot be carried forward to the next year.

Which loss can’t be carried forward to next subsequent year?

Capital Losses : Cannot be carried forward if the return is not filed within the original due date.

Which are the exceptions for set off and carry forward of losses?

However, there are certain exceptions to it: Loss of business acquired by inheritance (excl. unabsorbed depreciation) Accumulated business loss of Amalgamation/Demerger Company, fulfilling the conditions as laid down under section 72A/72AA of the Income-tax Act.

What are the losses which can be carried forward as per IT Act?

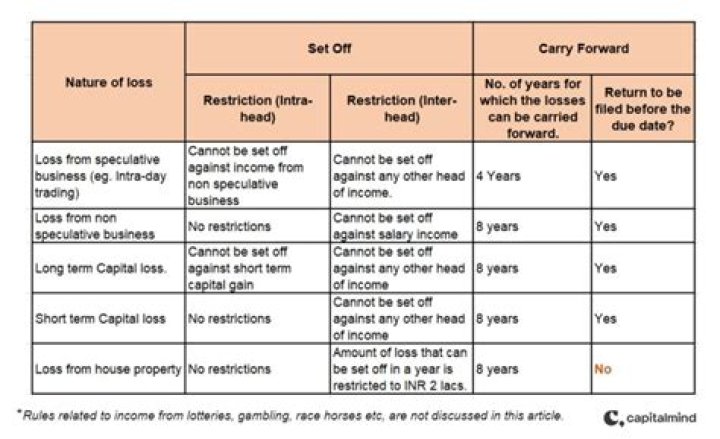

* It can be set off against any income in the year the loss is incurred. If the loss could not be set off in the year loss was incurred it can be carried forward up to 8 Assessment Years and loss will be allowed to set off against income under the head House Property.

Which loss Cannot be carry forward?

The following losses cannot be carried forward unless the return of income (for the year in which the loss is incurred) is submitted within the due date [of submission of return as given in section 139(1)]. loss (not being unabsorbed depreciation etc., from the activity of owning and maintaining race horses.

Can a loss be carried forward to the next tax year?

If you make a tax loss in an income year you can carry it forward and deduct it in future years against income for tax purposes.

When to use loss carryforward on income statement?

The loss, limited to 80% of income in the second year, can then be used in the second year as an expense on the income statement. It lowers net income, and therefore the taxable income, for that year to $1.2 million. A $200,000 deferred tax asset will remain on the balance sheet.

When do you claim loss on your tax return?

Losses. You generally make a tax loss when the total deductions you can claim for an income year exceed your income for the year. Total income includes both assessable and net exempt income for the year. If you make a tax loss in an income year you can carry it forward and deduct it in future years against income for tax purposes.

Where are losses carried forward in self assessment?

First off all, losses c/f (s385) must be offset against first available profits (as David says). These losses and offsets are entered on p3 of the self employment return (boxes 3.84 – 3.89). But there may be another alternative. This appears to be a new business.