Can the owner of a life insurance policy cash out?

Withdrawing Money From a Life Insurance Policy Generally, you can withdraw money from the policy on a tax-free basis, but only up to the amount you’ve already paid in premiums. Anything beyond the amount you’ve already paid in premiums typically is taxable.

How much do you get when you sell your life insurance policy?

If your policy is eligible to be sold, you can expect to receive from 10% to 35% of the amount that would be paid when you die. In certain situations, you could receive more. A few factors that will affect the amount you may be offered: The face value (coverage amount) of your policy.

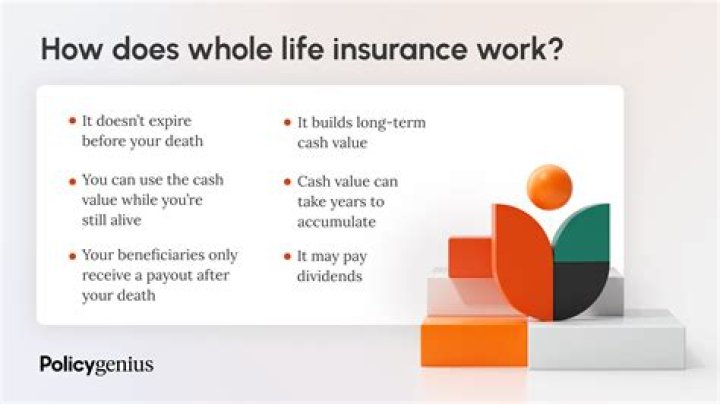

What happens to the cash value after the policy is fully paid up?

What happens to the cash value after the policy is fully paid up? The company plans to use the cash value to pay premiums until you die. The company could require you to resume paying premiums, or reduce the amount of the death benefit to an amount that the remaining cash value will support.

Are life insurance benefits tax free?

Answer: Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren’t includable in gross income and you don’t have to report them. However, any interest you receive is taxable and you should report it as interest received.

Who benefits from a life insurance policy?

You can choose to name a single beneficiary or a primary beneficiary and one or more contingent beneficiaries. A contingent beneficiary would receive death benefits from your life insurance policy if the primary beneficiary passes away. Minor children can’t be named as beneficiaries of a life insurance policy.

How to claim for sold life insurance compensation?

You can claim for the sold life policy number of different ways where the policy provider or broker may well have to address, either the policy and premiums that you have paid in their entirety through to having to conduct a review and proportionally refund monies if the policy was expensive or inappropriate for your needs.

How much does it cost to sell a life insurance policy?

Thus, assuming a sale of a policy for which $64,000 in premiums have been paid, with $10,000 of the premiums paid for the cost of insurance, the adjusted basis is $54,000. Assuming a cash surrender value of $78,000 and a sale price of $80,000, the difference between the $80,000 received and the $54,000 adjusted basis is gain.

How old do you have to be to sell your life insurance?

In summary, to be eligible to sell your life insurance policy, it is best to be over 65 years of age or have a serious medical condition and own a permanent (or convertible) life insurance policy that has a face value of at least $100,000. Why Sell your Life Insurance Policy?

How to find the number of life insurance policies sold?

The data can be adjusted to find the monthly sale of policies of a single life insurer. The data shows the number of policies sold by all life insurers in 2018-2020. It gives a clear idea of which life insurance company is leading the race of insuring the people.