Can you contribute to both a 401k and a Roth 401k?

If your employer offers both Roth and traditional 401(k) plans, typically you can chose to invest in both. Your total contributions cannot exceed the IRS limits ($19,000 in 2019 + $6,000 catch up for those 50 and older). But within this limit, you can invest a portion in a traditional plan and a portion in a Roth plan.

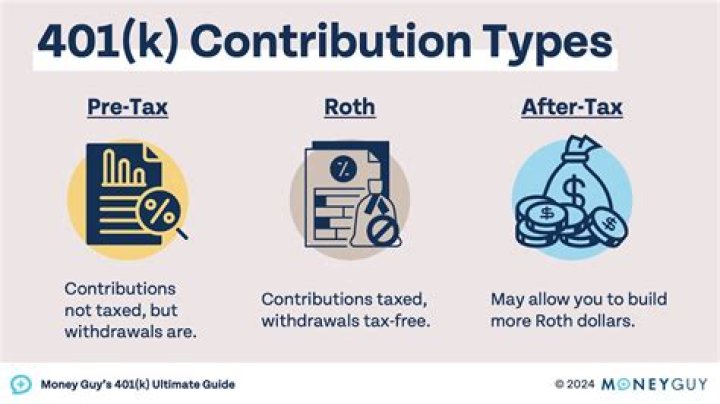

Is it better to contribute to a traditional 401k or Roth 401k?

The biggest benefit of the Roth 401(k) is this: Because you already paid taxes on your contributions, the withdrawals you make in retirement are tax-free. By contrast, if you have a traditional 401(k), you’ll have to pay taxes on the amount you withdraw based on your current tax rate at retirement.

Is a Roth 401k the same as a 401k?

The basic difference between a traditional and a Roth 401(k) is when you pay the taxes. With a traditional 401(k), you make contributions with pre-tax dollars, so you get a tax break up front, helping to lower your current income tax bill. With a Roth 401(k), it’s basically the reverse.

Should you split 401k between Roth and traditional?

In most cases, your tax situation should dictate which type of 401(k) to choose. If you’re in a low tax bracket now and anticipate being in a higher one after you retire, a Roth 401(k) makes the most sense. If you’re in a high tax bracket now, the traditional 401(k) might be the better option.

How much money can you put in a Roth 401k per year?

The contribution limit for a designated Roth 401(k) for 2020 and 2021 is $19,500. Account-holders who are age 50 or older may make catch-up contributions of up to $6,500, for a potential total annual contribution of $26,000.

Do employers match Roth 401k?

Yes, your employer can make matching contributions on your designated Roth contributions. Your employer must allocate any contributions to match designated Roth contributions into a pre-tax account, just like matching contributions on traditional, pre-tax elective contributions.

How much money can you put in a Roth 401 K?

The Roth 401(k) contribution limit for 2020 and 2021 is $19,500, but those aged 50 or over can also make a catch-up contribution of $6,500. Employers can contribute to employee Roth 401(k)s through a match or elective contributions.

What’s the difference between a 401k and a Roth IRA?

Employee contributions are made using after-tax dollars with no income limitations to participate. A Roth 401 (K) is a tax-advantaged retirement savings vehicle that combines features from traditional 401 (k) plans and Roth IRAs. Contributions and earnings can be withdrawn tax-free as long as certain criteria are met.

Can a 401k be rolled over to a Roth IRA?

For example, says Gething, “You can easily avoid required minimum distributions by rolling over your Roth 401 (k) to a Roth IRA.” And If you happen to be searching for the best place to get one of these accounts, Investopedia has created a list of the best brokers for IRAs .

Are there income limits on a Roth 401k?

If your employer offers it, you’re eligible. Unlike a Roth IRA, a Roth 401 (k) has no income limits. That’s a fantastic feature of the Roth 401 (k). No matter how much money you earn, you can contribute to a Roth 401 (k).

Can a company match a Roth 401k contribution?

Employers can match your contributions to a Roth 401(k) – they’re actually offered a tax incentive to do so. But keep in mind that those matching funds and their earnings will be placed in a pre-tax account and taxed once you start taking distributions.