Do buyer and seller have to agree on purchase price allocation?

In the asset purchase agreement, the buyer and seller must agree on the allocation of the purchase price, and it must be reported accordingly on IRS Form 8594.

How does allocation of purchase price affect taxes?

The asset classes the purchase price is allocated to dictates the applicable tax rates on any gains and losses. For example, gains and losses attributable to inventory (Class IV) are treated as ordinary income. Gains attributable to goodwill (Class VII), on the other hand, are treated as capital gains/losses.

Is a purchase price allocation required?

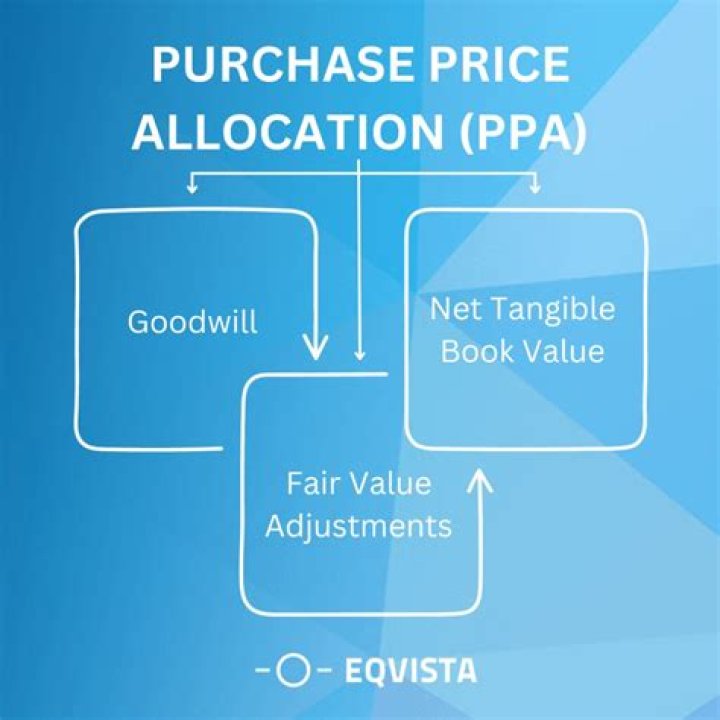

A Purchase Price Allocation (“PPA”) is frequently required for tax and financial reporting following a merger or acquisition . However, a PPA can be much more than just an accounting exercise.

Why do a purchase price allocation?

Purchase price allocations help to accurately reflect value drivers for an acquired business and help financial statement users understand what each part of the purchased business is worth. It is important to highlight that not all acquired targets are subject to being recorded as a business combination.

How do you allocate Purchase Price in an asset sale?

In a non-stock sale, the usual principle is that the purchase price of the company’s assets should be allocated based on fair market value. The buyer and the seller will negotiate the allocation of purchase price for these assets so that neither party is disadvantaged by the sale.

How do you prepare purchase price allocation?

5 Key Steps to Prepare a Purchase Price Allocation After A Business Combination

- Step 1: Determine the Fair Value of Consideration Paid.

- Step 2: Revalue all Existing Assets and Liabilities to their Acquisition Date Fair Values.

- Step 3: Identify Intangible Assets Acquired.

When to use purchase price allocation for tax purposes?

For instance, buyers will receive a larger tax benefit if the purchase price is allocated more to fixed assets that depreciate over 5 to 7 years versus goodwill or non-compete agreements, which will amortize over 15 years (for tax purposes only).

How to allocate the purchase price of furniture?

Purchase Price Allocation Furniture Purchase Price 50,000 Accumulated Depreciation 40,000 Tax Book Value 10,000 Price Allocation to Asset 65,000 Tax Book Value 10,000

How to allocate money when selling or buying a business?

When you sell or buy a business, you are required to “allocate” the purchase price to each of these seven different asset classes. So, for example, if the purchase price is $200,000, you might allocate $30,000 to equipment, $20,000 to inventory and $50,000 to intangibles, with the $100,000 balance allocated to goodwill.

How does sales tax affect the purchase price?

Most sellers will want the buyer to simply back out sales tax from the purchase price. So, if a $500,000 deal would incur $10,000 in sales tax, the buyer is essentially paying $510,000 since the seller still wants $500,000 in proceeds. Sales tax will vary by state and by purchase price allocation,…