Do dividends reduce earnings and profits?

Although distributions of cash or property to the shareholders will reduce the corporation’s earnings and profits (E&P), such distributions will not reduce the corporation’s taxable income. The corporation pays tax on the taxable income, and the shareholders pay tax on dividends received.

How are earnings and profits calculated?

Earnings & profits (E&P) is the measure of a corporation’s economic ability to pay dividends to its shareholders. In general, a corporation’s current-year E&P is calculated by making adjustments to its taxable income for the year for items that are treated differently for E&P purposes.

Why is E&P important?

E&P is used to determine whether any distributions are a taxable dividend, a tax free return of capital or a capital gain. Due to the lack of a statutory definition, one needs to look at the regulations, administrative guidance and other sources to determine it accurately.

How does current earnings and profits differ from accumulated earnings and profits?

Current earnings and profits represents the corporation’s earnings and profits of the current year before reduction by any distributions made during the year. Accumulated earnings and profits represents undistributed earnings and profits from all years prior to the current year.

Are dividends taxable when declared or paid?

A spillover dividend is a dividend that is announced in one year, but counted as part of another year’s income for federal tax purposes. In these cases, the dividend would count as taxable income in the year that it was declared, not the year in which it was paid.

Are dividends paid from profit before tax?

Corporations pay taxes on their earnings and then pay shareholders dividends out of the after-tax earnings. Shareholders receiving dividend payments from a company must then pay taxes on that income as part of their personal income taxes.

What are current earnings and profits?

Current earnings and profits, if not paid out, become accumulated earnings (profits) tax. A distribution comes first from current earnings and profits and then from accumulated earnings and profits and is taxable to the shareholder to the extent of current and accumulated earnings and profits.

What does earnings and profits include?

Accumulated earnings and profits (E&P) is an accounting term applicable to stockholders of corporations. Accumulated earnings and profits are a company’s net profits after paying dividends to the stockholders, serving as a measure of the economic ability of a corporation to pay such cash distributions.

What is AE&P?

The term “retained earnings” refers to a corporation’s undistributed earnings; its computation is normally governed and determined by generally accepted accounting principles (GAAP). AE&P is also a measure of the undistributed earnings of a corporation, but from a tax point of view.

Can you have negative accumulated earnings and profits?

If the current E&P equals or exceeds the amount of the distribution, it is a fully taxable dividend to the shareholder even if the corporation has negative accumulated E&P (Regs. In other words, if there is sufficient current E&P to cover all distributions made during the year, all distributions are taxable dividends.

What is the difference between accumulated profit and retained earnings?

When finance people talk about “retained earnings,” “accumulated profits,” “undistributed income,” and “income reserve,” they mean the same thing. Think of this as income the business has set aside since its inception. Net income increases a company’s income reserve whereas net loss lowers it.

Can earnings and profits be negative?

Cash distributions reduce E&P. Note Page 4 Distributions cannot create a deficit in E&P, but E&P can have a negative balance due to net operating losses (negative taxable income). 2.

Thus, a corporation’s E&P should include all items of income, gain, loss or deduction resulting from the economic activities of the corporation, regardless of the treatment of such items in computing taxable income or retained earnings.

A Company pays Corporation Tax on its profits before dividends are paid out. Consequently, shareholders are treated as having already paid tax on their dividends (called a ‘tax credit’). A shareholder who is paying Higher Rate Tax will have the dividends added to their income and will have extra tax to pay.

What is E and P?

How are dividends and profits treated in taxes?

• Distributions from corporate earnings and profits (E & P) are treated as a dividend distribution, taxed as ordinary income • Distributions in excess of E & P are nontaxable to extent of shareholder’s basis (i.e., a return of capital) • Excess over basis is capital gain • Distributions from corporate earnings and

Why is it important to calculate earnings and profits?

Earnings & profits (E&P) is the measure of a corporation’s economic ability to pay dividends to its shareholders. An up-to-date E&P calculation is important for many corporate transactions, including determining whether a distribution to shareholders is a taxable dividend.

What’s the difference between earnings per share and dividends per share?

Earnings per share is a ratio that gauges how profitable a company is per share of its stock. Dividends per share, on the other hand, calculates the portion of a company’s earnings that is paid out to shareholders.

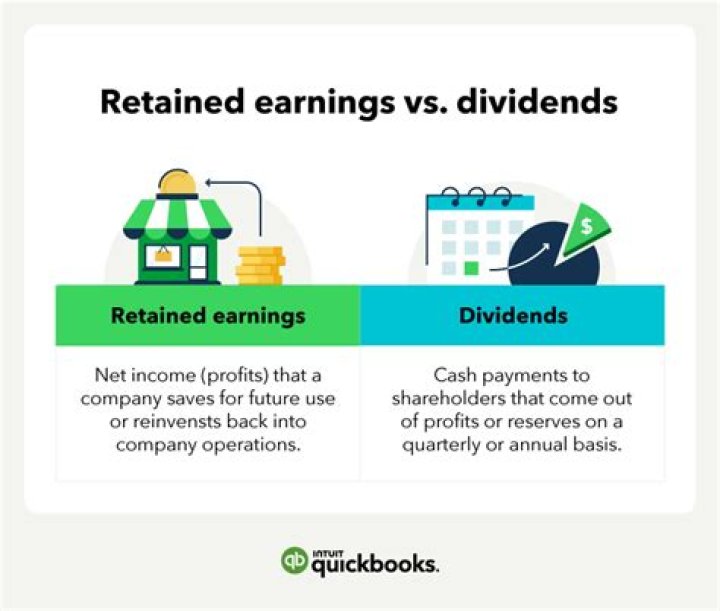

What makes up the retained earnings of a dividend?

What is a Dividend? A dividend is a share of profits and retained earnings Retained EarningsThe Retained Earnings formula represents all accumulated net income netted by all dividends paid to shareholders. Retained Earnings are part that a company pays out to its shareholders.