Do notes receivable have a fixed maturity date?

A note receivable is a formal promise in writing to pay a specific amount of money on a specified date or dates, made between a borrower (the one who borrows money) and a lender (the one who lends money). If it states that the term of the note is in months, then the maturity date is simply counted on months.

How do you find the maturity value of a note receivable?

It can then be simplified to find the answer. When you divide, multiply, and add it up, you’ll find that the maturity value of this note is $102,000. That is the maturity value of the note — the amount the borrower will have to pay to the bank when the note comes due.

How long are notes receivable?

Notes receivable are classified as long-term or short-term, depending on the duration. Notes receivable that are due more than one year after the date recorded on a balance sheet must be reported as long-term assets.

How do you calculate notes receivable?

In order to calculate interest receivable and interest revenue for notes receivable, you can multiply the interest rate by the amount of notes receivable and then divide by 12 to capture the monthly rate.

Is notes receivable a credit or debit?

The payee should record the interest earned and remove the note from its Notes Receivable account. Thus, the payee of the note should debit Accounts Receivable for the maturity value of the note and credit Notes Receivable for the note’s face value and Interest Revenue for the interest.

What is the difference between notes receivable and notes payable?

Notes Receivable vs Notes Payable Notes Payable is a liability as it records the value a business owes in promissory notes. Notes Receivable are an asset as they record the value that a business is owed in promissory notes.

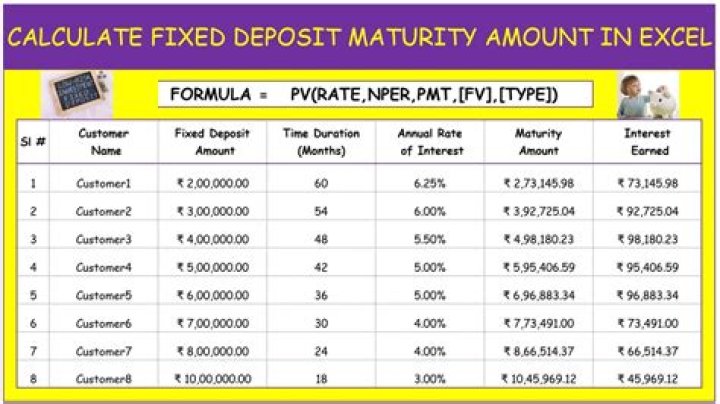

What is the formula of maturity value?

The maturity value formula is V = P x (1 + r)^n. You see that V, P, r and n are variables in the formula. V is the maturity value, P is the original principal amount, and n is the number of compounding intervals from the time of issue to maturity date. The variable r represents that periodic interest rate.

How do you record interest in notes receivable?

Calculate the Amount of Interest To determine the amount of interest, multiply the total note receivable amount by 10 percent (5000 x 10% = $500). In order to record the interest that is earned during the accounting period, you also need to calculate the interest that is earned daily.

What is included in notes payable?

Notes payable is a liability account where a borrower records a written promise to repay the lender. Recording notes payable includes specifying details of the matter. Information in the written statement generally includes the principal amount borrowed, the due date of payment and the interest to be paid.

What is notes receivable classified as?

Summary. A note receivable is also known as a promissory note. When the note is due within less than a year, it is considered a current asset on the balance sheet of the company the note is owed to. If its due date is more than a year in the future, it is considered a non-current asset.

Is notes receivable a permanent account?

Examples of permanent accounts are: Asset accounts including Cash, Accounts Receivable, Inventory, Investments, Equipment, and others. Liability accounts such as Accounts Payable, Notes Payable, Accrued Liabilities, Deferred Income Taxes, etc.

Is note receivable an asset?

Notes Receivable are an asset as they record the value that a business is owed in promissory notes.

What is note receivable example?

The notes receivable is an account on the balance sheet usually under the current assets section if its life is less than a year. Specifically, a note receivable is a written promise to receive money at a future date. The money is usually made up of interest and principal.

Is a note receivable to be collected in two years a current asset?

If the note receivable is due within a year, then it is treated as a current asset on the balance sheet. If it is not due until a date that is more than one year in the future, then it is treated as a non-current asset on the balance sheet.

MV = P * ( 1 + r )n MV is the Maturity Value. P is the principal amount. r is the rate of interest applicable. n is the number of compounding intervals since the time of the date of deposit till maturity.

When do notes receivables need to be paid?

Due (maturity) date is the date when the note receivable is to be paid. As mentioned earlier, notes receivable require an interest payment by the maker of the note. Notes receivable usually state the annual interest rate, regardless of the term of the note. Interest can be paid monthly, quarterly, semiannually, or annually.

What is the maturity value of a note?

To calculate the maturity of this note, we use a simple formula: Maturity value = Principal x (1+ Rate x Time) In this case, we need to be sure that the annual rate of interest is adjusted for the fact that the note is shorter than a full year.

Which is an example of a maturity date?

An example of a note’s maturity value Suppose a company signed a promissory note to borrow $100,000 from a local bank. The note will mature in 90 days and carries an annual rate of interest of 8%.

When does a note receivable become a non-current asset?

Key Takeaways. A note receivable is also known as a promissory note. When the note is due within less than a year, it is considered a current asset on the balance sheet of the company the note is owed to. If its due date is more than a year in the future, it is considered a non-current asset.