Do rental losses reduce AGI?

Modified Adjusted Gross Income If a taxpayer’s MAGI is $100,000 or less for the tax year, the taxpayer can deduct up to $25,000 of rental loss. Taxpayers may also be able to take a reduced amount of the rental loss if their MAGI is more than $100,000.

Does rental property loss reduce taxable income?

Rental property losses are considered passive losses, which means they can only be deducted from passive income. If you don’t have enough in rental income for the tax year to offset your losses, you should be able to carry the excess over to a future year.

Can you deduct rental property losses against ordinary income?

Federal tax law provides that up to $25,000 of losses associated with real estate rental activities can be netted against ordinary income. The key to claiming real estate losses from rental property is to qualify by actively participating in rental activity.

Can you write off lost rental income?

You can even write off a net loss on a rental home as long as you meet income requirements, own at least 10% of the property, and actively participate in the rental of the home. If your modified adjusted gross income is below $100,000, you can deduct the full $3,000 loss.

Does AGI include net rental income?

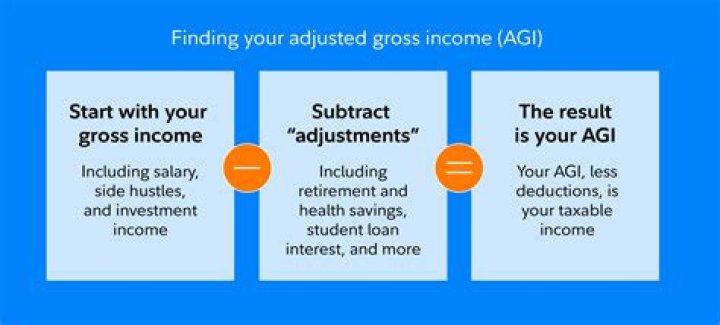

In the United States income tax system, adjusted gross income (AGI) is an individual’s total gross income minus specific deductions. It includes wages, interest, dividends, business income, rental income, and all other types of income.

Can you use rental losses to offset AGI?

As such, you can use rental losses to offset money that you earn from being a broker, property manager or professional investor without any limitation tied to your AGI. Getting qualified as a real estate professional isn’t as easy as simply getting a real estate broker’s license.

Who is eligible for rental real estate loss allowance?

The rental real estate tax loss allowance is available only to property owners who actively participate in the management of the property. To meet the active participation test, the taxpayer must make management decisions for the property. 2 It is possible to meet the test even if the property is run by a management company.

How much can you claim as loss on rental property on taxes?

The rental real estate loss allowance is a federal tax deduction available to taxpayers who own and rent property in the U.S. Up to $25,000 may be deducted as a real estate loss per year as long as the individual’s adjusted gross income is $100,000 or less.

Can you deduct rental losses as passive income?

Thus, for example, you’d have passive income if you earn a profit from one or more rentals. Without passive income, your rental losses become suspended losses you can’t deduct until you have sufficient passive income in a future year or sell the property to an unrelated party. You may not be able to deduct such losses for years.