Do you pay taxes on distributions from a partnership?

Generally, there are no tax consequences of a current property distribution — there is never a taxable gain or loss, either to the partnership or to the partner. Since the amount of cash received is less than your interest in the partnership, there is no taxable transaction.

Are LLC capital distributions taxable?

You are taxed on how much money the LLC makes, period. Putting money into or taking money out of the LLC is not a taxable event.

Do you pay taxes on k1 distributions?

Although withdrawals and distributions are noted on the Schedule K-1, they generally aren’t considered to be taxable income. Partners are taxed on the net income a partnership earns regardless of whether or not the income is distributed.

How are distributions taxed?

Any distributions will be a tax-free reduction of the shareholder’s basis. Any distribution in excess of the shareholder’s stock basis is treated as capital gain from the deemed disposition of stock.

How are distributions from a LLC and partnership taxed?

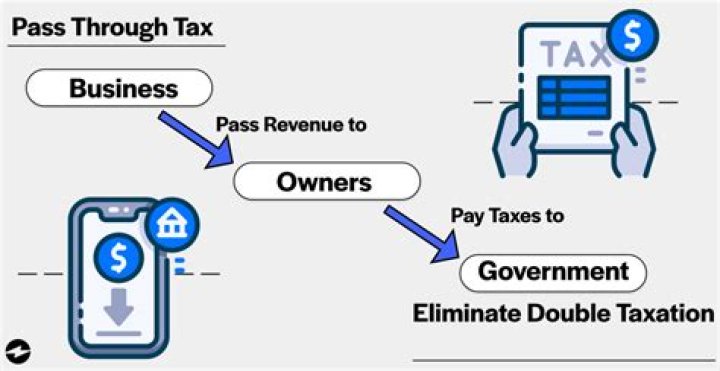

Tax Consequences of Distributions from LLCs and Partnerships Unlike the rules that apply to C corporations, which tax income both at the entity and at the owner level, the partnership rules are designed to only tax income once, at the owner level.

How are earnings distributed to partners in a partnership?

Earnings are distributed to each partner’s capital account from which distributions are charged against. However, certain types of distributions and any distributions exceeding the partner’s basis may result in gains or losses that must be reported for the year when they occur.

When do general partners have to make tax distributions?

Tax Distributions. Subject to §17-607 of the Act, and unless determined otherwise by the General Partner in its sole discretion, the Partnership shall make distributions to each Partner for each calendar quarter ending after the date hereof as follows (collectively, the “Tax Distributions”): Tax Distributions.

How are property distributions treated in a partnership?

Property Distributions. When property is distributed to a partner, then the partnership must treat it as a sale at fair market value (FMV). The partner’s capital account is decreased by the FMV of the property distributed. The book gain or loss on the constructive sale is apportioned to each of the partners’ accounts.