Do you recommend refinancing?

One of the best reasons to refinance is to lower the interest rate on your existing loan. Historically, the rule of thumb is that refinancing is a good idea if you can reduce your interest rate by at least 2%. However, many lenders say 1% savings is enough of an incentive to refinance.

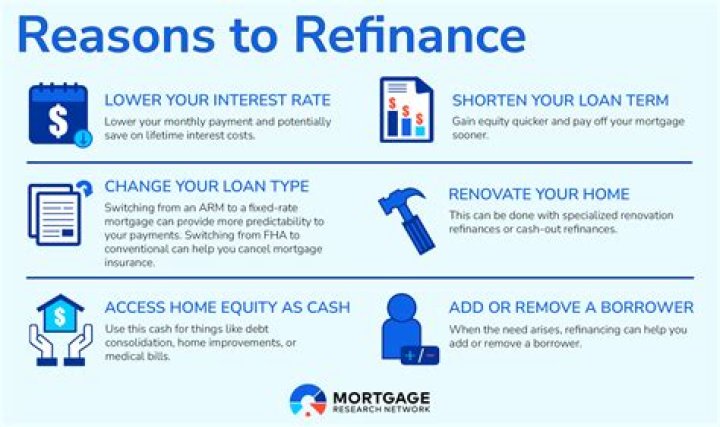

How can you decide whether you should refinance the house?

Although every situation is different, I would recommend refinancing your mortgage if:

- Current interest rates are at least 1% lower than your existing rate.

- You plan on staying in your home for another 5 years (give or take)

- You anticipate being approved for the refinance loan.

What to do if refinance is taking too long?

Here are a few ways you can make the refi process as smooth as possible:

- Get your paperwork in order. Don’t let something simple like a missing document delay your refinance.

- Make sure the lender will honor your rate lock.

- Keep your credit score tight.

What documents do I need to refinance my home?

Refinance Required Documentation Checklist

- Pay Stubs. When applying for a home loan refinance, your lender will need proof of income.

- Tax Returns and W-2s and/or 1099s.

- Credit Report.

- Statements of Outstanding Debt.

- Statement of Assets.

Why is my refinance taking forever?

Are you wondering why does it take so long to refinance a mortgage? The simple answer is because lending standards have tightened tremendously since the financial crisis. The banking sector lent too loosely before the crisis. As a result, regulators locked down.

What should I know before refinancing my mortgage?

It is important to check with your current lender before starting the refinance process and potentially losing money. When considering refinancing, it is vital to determine if this action will you save money. Generally, only contemplate refinancing if you can decrease your current mortgage rate by a full percent.

Is there a limit to how often you can refinance your mortgage?

There’s no legal limit on the number of times you can refinance your home loan. However, mortgage lenders do set a few rules that dictate the frequency of refinancing by loan type, and there are some special considerations to note if you want a cash-out refinance. Remember: You need to have equity built up to take cash out against it.

How much equity do you have after refinancing your home?

In the years after your refinance, you’ve paid only $2,000 off your principal after accounting for interest. Though your loan balance is now $128,000, you only have $22,000 worth of equity in your home. Most lenders only allow you to refinance 80% – 90% of your loan value.

What happens if I refinance my home loan again?

Your current loan already accounts for the costs of your last refinance. If you refinance again, your new savings are added to the savings received in your current refinancing. There are many mortgage refinance break-even calculators available online.