Does CAPM calculate expected return?

The expected return of the CAPM formula is used to discount the expected dividends and capital appreciation of the stock over the expected holding period. If the discounted value of those future cash flows is equal to $100 then the CAPM formula indicates the stock is fairly valued relative to risk.

Should CAPM be higher than expected return?

The CAPM formula yields the expected return of the security. A security with a beta higher than 1.0 carries greater systematic risk and volatility than the overall market, and a security with a beta less than 1.0, has less systematic risk and volatility than the market.

Why does CAPM fail?

Research shows that the CAPM calculation is a misleading determination of potential rate of return, despite widespread use. The underlying assumptions of the CAPM are unrealistic in nature, and have little relation to the actual investing world.

Are there any problems with the CAPM model?

A problem arises when, at any given time, the market return can be negative. As a result, a long-term market return is utilized to smooth the return. Another issue is that these returns are backward-looking and may not be representative of future market returns.

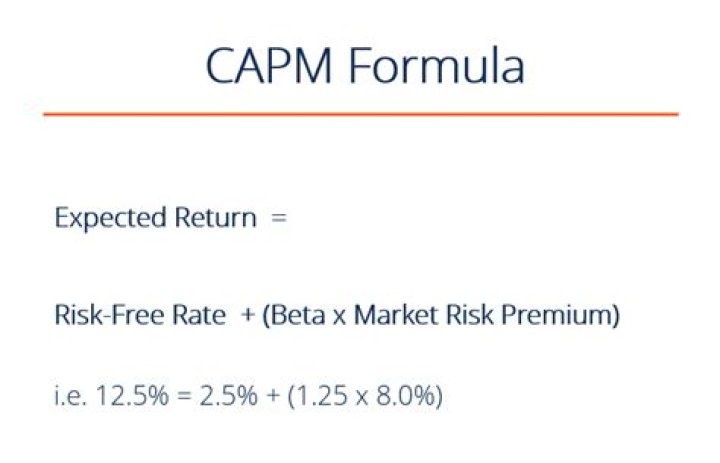

How to calculate expected return in CAPM formula?

Let’s break down the answer using the formula from above in the article: 1 Expected return = Risk Free Rate + [Beta x Market Return Premium] 2 Expected return = 2.5% + [1.25 x 7.5%] 3 Expected return = 11.9% More …

What does CAPM mean in capital asset pricing model?

What is CAPM? The Capital Asset Pricing Model (CAPM) is a model that describes the relationship between the expected return and risk of investing in a security. It shows that the expected return on a security is equal to the risk-free return plus a risk premium

How is the risk free rate of return used in CAPM?

To use the CAPM, values need to be assigned to the risk-free rate of return, the return on the market, or the equity risk premium (ERP), and the equity beta. The yield on short-term government debt, which is used as a substitute for the risk-free rate of return, is not fixed but changes regularly with changing economic circumstances.