Does cash basis accept accounting?

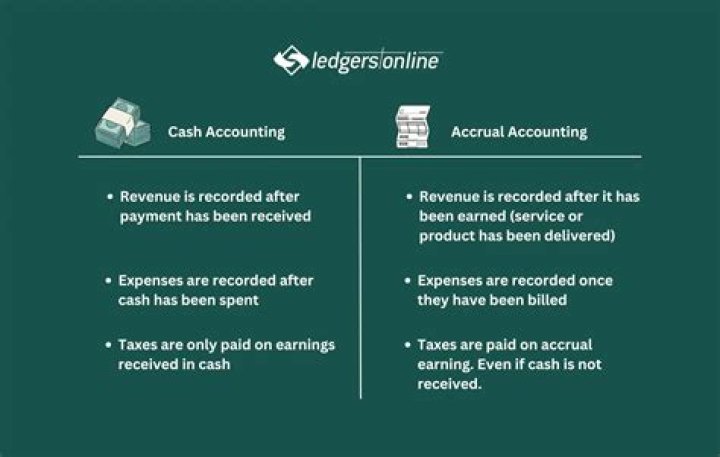

Cash basis accounting is an accounting system that recognizes revenues and expenses only when cash is exchanged. Cash basis accounting is not acceptable under the generally Acceptable Accounting Principles (GAAP) or the International Financial Reporting Standards (IFRS).

Which entities can use cash basis of accounting?

You can use the cash accounting method if any of the following applies:

- you are a small business entity – that is, an individual, partnership, trust or company with an aggregated turnover of less than $10 million.

- you are not carrying on a business, but your enterprise’s GST turnover is $2 million or less.

Is cash basis accounting allowed under IFRS?

The modified cash basis is not allowed under Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS), which means that a business using this basis will need to alter the recordation of those elements of its transactions that were recorded under the cash basis, so that they …

What are the disadvantages of cash basis of accounting?

One disadvantage of cash-basis accounting is that it gives your business a limited look at your income and expenses. Cash basis does not show your business’s liabilities. As a result, you may think you have more money to spend than you actually have.

When do you use a cash basis for Hoa?

When recording on a Cash Basis, the “Cash” account title increases on the Balance Sheet. Since all transactions are on a cash basis, account titles like “Assessments Receivable” or “Prepaid Assessments” aren’t used. The same HOA accounting rules apply for recording expenses when using the Cash Basis.

What kind of accounting does a homeowners association use?

In most states, homeowners associations can choose one of three basis of accounting to prepare interim statements: These accounting methods will be used to prepare several important financial reports for the homeowners association. The most important are the following: Balance Sheet.

When do you use cash basis of accounting?

Using the Cash Basis of Accounting, you record income and expenses when money changes hands. That means you only report transactions when you pay for them or receive payment for them. Using this method, no such account titles like Assessments Receivable or Accounts Payable appear on your financial statements.

How are financial statements prepared for a homeowners association?

There are several methods that may be used to prepare your HOA’s financial statements. In most states, homeowners associations can choose one of three bases of accounting to prepare interim statements: These accounting methods will be used to prepare several important financial reports for the homeowners association.