Does OAA affect shareholder basis?

The OAA reconciles those items that increase or decrease a shareholder’s stock basis but not AAA, primarily tax-exempt income and deductions attributable to tax-exempt income.

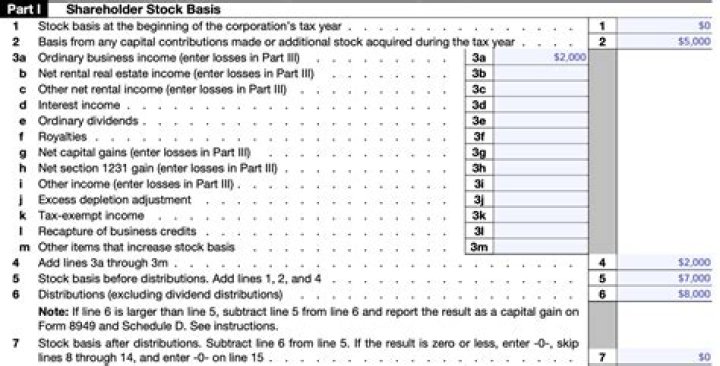

Which of the following are increases to a shareholder’s basis in an S corporation?

Contributions to the S corporation Reason: Contributions to the S corporation increase the contributing shareholder’s basis. Shareholder’s share of separately stated items of income or gains Reason: The share of income or gains increases the S corporation shareholder’s basis.

Is AAA the same as shareholder basis?

Each year, an S corporation must adjust its AAA in a manner similar to a shareholder’s required adjustments to stock basis. Unlike stock basis, however, AAA is a corporate-level attribute and is generally unaffected by shareholder-level transactions such as sales or exchanges.

How to reconstruct the basis of an S corporation?

The difficultly in reconstructing basis comes down to what records are available. The best and only way to truly know your basis is correct is to go back to the S election date (or date your first acquired stock in the S corporation) and roll forward from the beginning.

When does a shareholder have basis in S corporation debt?

The debt must be “directly” from the shareholder to the S corporation. The shareholder must have an actual “economic outlay.” A shareholder has basis in a loan if he or she makes a direct loan to the S corporation. If the shareholder merely guarantees the debt of the S corporation, the shareholder does not have basis in debt to the S corporation.

Is it the responsibility of the corporation to track shareholder basis?

The concept of shareholder basis is somewhat simple, however the calculation can be cumbersome if it was not properly tracked by the shareholder over the years. It is important to note that it is not the corporation’s responsibility to track a shareholder’s stock and debt basis, but rather it’s the shareholder’s responsibility.

How does computing stock basis work for S corporation?

Computing Stock Basis In computing stock basis, the shareholder starts with their initial capital contribution to the S corporation or the initial cost of the stock they purchased (the same as a C corporation). That amount is then increased and/or decreased based on the pass-through amounts from the S corporation.