Does the fact that the unadjusted trial balance is balanced mean that there are no errors in the accounts?

If the total debits equal the total credits, the trial balance is considered to be balanced, and there should be no mathematical errors in the ledgers. However, this does not mean there are no errors in a company’s accounting system.

Does unadjusted trial balance have to equal?

Format of unadjusted trial balance The total of the debit column of the unadjusted trial balance must be equal to the total of the credit column. If they aren’t in agreement, it means that the trial balance has been prepared incorrectly or the journal entries have not been transferred to the ledger accounts accurately.

What if trial balance is not equal?

The trial balance has two sides, the debit side and the credit side. Debits include accounts such as asset accounts and expense accounts. Credits are accounts such as income, equity and liabilities. A trial balance will not balance if both sides do not equal, and the reason has to be explored and corrected.

When a journal entry is posted twice this will cause the trial balance to?

Posting a transaction twice will cause the trial balance totals to be equal. Transactions are listed in the journal chronologically. The chart of accounts should be the same for each business. A transaction that is recorded in the journal is called a journal entry.

Which of the following statements about trial balance is incorrect?

If wrong entry are passed with same amount in debit and credit, trail balance still agrees. A trial balance proves that no error of any kind has been made in the accounting for the activities of a period is incorrect.

Which comes first adjusting entries or trial balance?

An adjusted trial balance is created after all adjusting entries have been posted into the appropriate general ledger account. The adjusted trial balance is completed to ensure that the period ending financial statements will be accurate and in balance.

What is the difference between trial balance and adjusted trial balance?

Difference Between Trial Balance and Adjusted Trial Balance Trial balance excludes entries like accrued expense. read more, accrued revenue, prepayment, and depreciation, whereas adjusted trial balance includes the same. A trial balance is a list of closing balances of ledger account on a particular point of time.

How can a balanced trial balance still have errors?

Trial balance errors

- Entries made twice. If an entry is made twice, the trial balance will still be in balance, so that is not a good document for finding it.

- Entries not made at all.

- Entries to the wrong account.

- Reversed entries.

- Transposed numbers.

- Unbalanced entries.

The purpose of a trial balance is to prove that the value of all the debit value balances equals the total of all the credit value balances. If the total of the debit column does not equal the total value of the credit column then this would show that there is an error in the nominal ledger accounts.

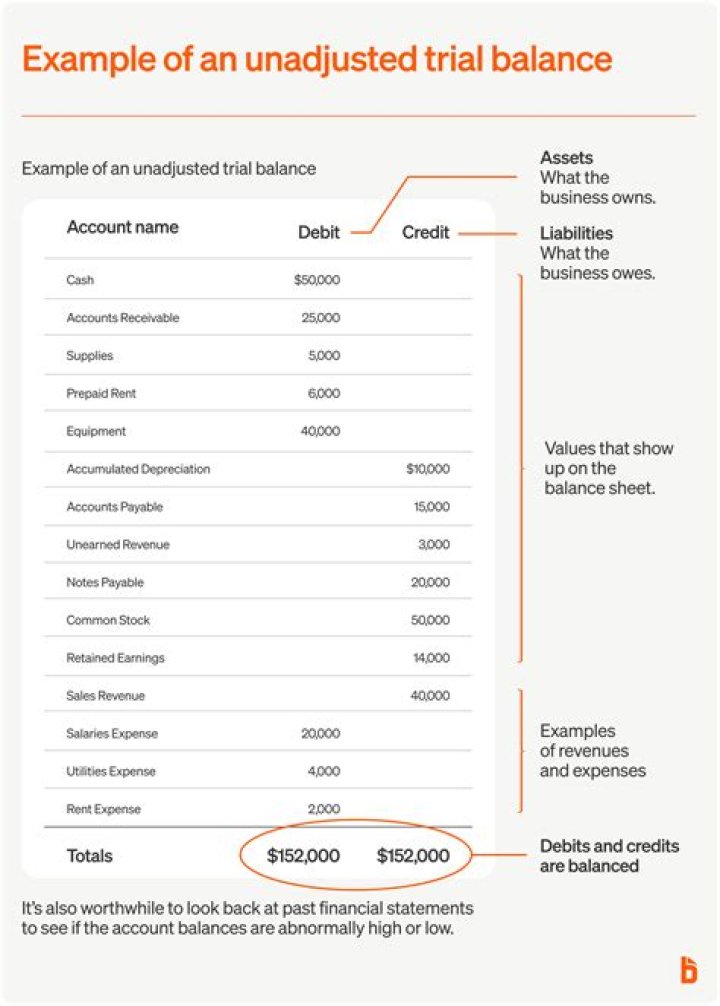

What does unadjusted trial balance mean in accounting?

An unadjusted trial balance is a listing of all the business accounts that are going to appear on the financial statements before year-end adjusting journal entries are made.

How are account balances listed on a trial balance?

First, the account balances from the general ledger and subsidiary ledgers are transferred to a trial balance. Next, these balances are listed in balance sheet and income statement order with their debit and credit balances. The beginning trial balance or unadjusted trial balance simply lists the unadjusted balances for each account.

How is the unadjusted balance on a balance sheet calculated?

Format. Most charts of accounts are numbered in balance sheet order, so the unadjusted trial balance also displays the account numbers in balance sheet order starting with the assets , liabilities, and equity accounts and ending with income and expense accounts. Both the debit and credit columns are calculated at the bottom of a trial balance.

What to do if trial balance is not tallied?

Enlist the accounts and write the balances in respective debit and credit columns. If the total of both sides is the same, the trial balance is mathematically correct. In case the same is not tallied, look for errors and reasons and correct the same.