How can I find out what tax deductions I can claim?

Find out which deductions, credits, and expenses you can claim to reduce the amount of tax you need to pay. There are a few ways to do this: Did you find what you were looking for?

What kind of deductions can I take on my taxes?

1 Traditional IRA deduction 2 HSA/FSA deduction 3 Dependent care FSA contributions 4 Student loan interest deduction 5 Teacher classroom expenses 6 Self-employed tax deductions 7 Alimony deduction 8 Moving expense deduction (for armed forces)

Are there restrictions on the use of pretax deductions?

Pretax deductions are a powerful tool to reduce your income tax, but not all pretax deductions are made equal. These deductions have restrictions, so check with a tax professional before processing payroll that includes them. You can find a list of pretax deductions and restrictions in IRS Publication 15, Section 15.

Are there any tax deductions that low income people can claim?

Low-income taxpayers can deduct up to 50% of their contributions to a SIMPLE, SEP, traditional or Roth IRA, 401 (k), 403 (b), governmental 457 (b) plan, or ABLE account. The maximum saver’s credit available is $4,000 for joint filers and $2,000 for all others. Use Form 8880 and Form 1040 Schedule 3 to claim the saver’s credit.

What are the most common forms of pretax deductions?

The most common forms of pretax deductions are health insurance and retirement plan contributions, though several more exist. Pretax deductions can get quirky. The IRS dictates what qualifies as a pretax deduction for each tax, and it’s not always the same.

What are all of the tax deductions and credits?

All deductions, credits, and expenses. 1 Adult basic education tuition assistance. 2 Employees of prescribed international organizations. 3 Exempt foreign income. 4 Vow of perpetual poverty Taxable income education-filter 26000 Taxable income Taxable income 30000 Basic personal amount Federal non-refundable tax

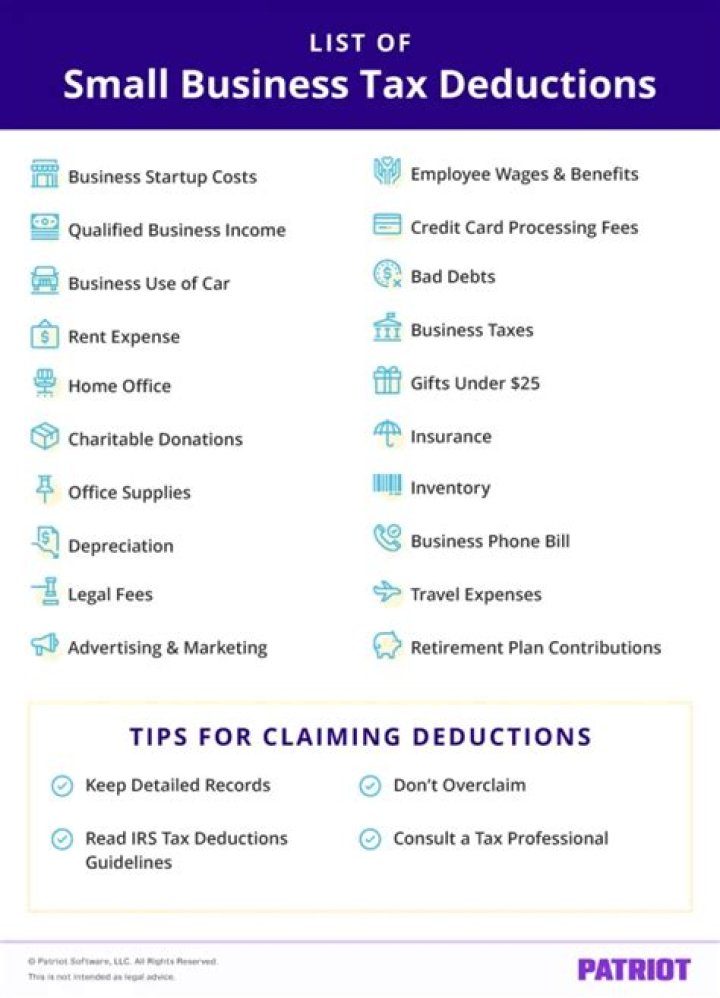

What kind of deductions can I claim on my business taxes?

Loans taken out for business purposes, including mortgages on business real estate or lines of credit obtained for business purchases, may qualify for tax deduction. The taxpayer must be legally liable for the acquired debt. The taxpayer and the lender have a true debtor-creditor relationship.