How do I account for deferred income tax?

Recording a deduction on your financial statements in the first year that is not taken until the next year’s tax return creates a deferred tax asset on the balance sheet. If you recognize revenue in the first year and pay the corresponding tax the next year, you would record a deferred tax liability.

How are deferred taxes recorded on the balance sheet?

Deferred income tax shows up as a liability on the balance sheet. The difference in depreciation methods used by the IRS and GAAP is the most common cause of deferred income tax. Deferred income tax can be classified as either a current or long-term liability.

How does a deferred tax liability arise?

In simple words, Deferred tax liabilities are created when income tax expense (income statement item) is higher than taxes payable (tax return), and the difference is expected to reverse in the future. DTL is the amount of income taxes that are payable in future periods as a result of temporary taxable differences.

How do you account for a deferred liability?

Since deferred revenues are not considered revenue until they are earned, they are not reported on the income statement. Instead they are reported on the balance sheet as a liability. As the income is earned, the liability is decreased and recognized as income.

What is the journal entry for a deferred tax liability?

The book entries of deferred tax is very simple. We have to create Deferred Tax liability A/c or Deferred Tax Asset A/c by debiting or crediting Profit & Loss A/c respectively. The Deferred Tax is created at normal tax rate.

What does deferred tax liability mean in accounting?

A deferred tax liability is a liability to future income tax. For any given accounting period the amount of income a business is taxed on is set out in its tax return, and is based on rules established by the tax authorities.

Where does deferred tax go on the balance sheet?

Deferred income tax shows up as a liability on the balance sheet. The difference in depreciation methods used by the IRS and GAAP is the most common cause of deferred income tax. Deferred income tax can be classified as either a current or long-term liability. Generally accepted accounting principles (GAAP) guide financial accounting practices.

What’s the difference between deferred income tax and Gaap?

The difference in depreciation methods used by the IRS and GAAP is the most common cause of deferred income tax. Deferred income tax can be classified as either a current or long-term liability. Generally accepted accounting principles (GAAP) guide financial accounting practices.

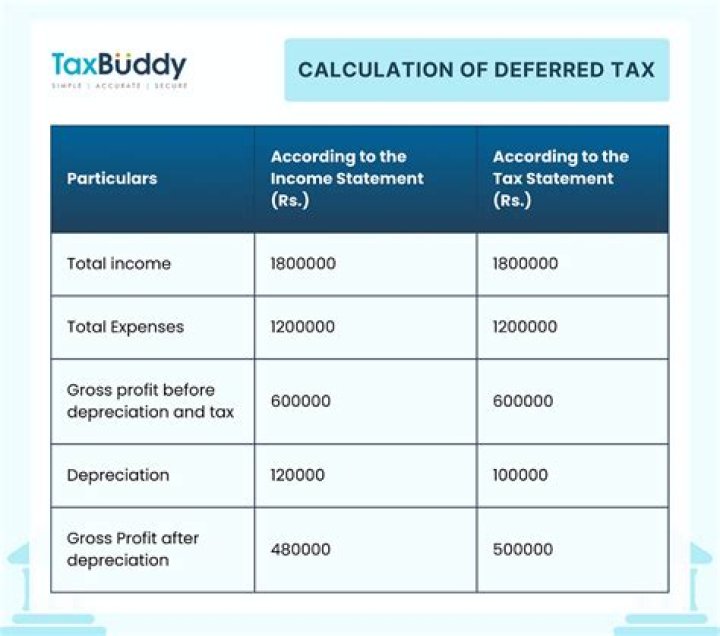

What happens to deferred taxes at the end of the life of the asset?

At the end of the life of the asset, no deferred tax liability exists, as the total depreciation between the two methods is equal. A deferred income tax liability results from the difference between the income tax expense reported on the income statement and the income tax payable, which is on the balance sheet.