How do I record a discount on notes payable?

Discounted notes use the discount on notes payable account to record the discount and keep track of it was the note is repaid. The discount account is a contra liability account with a debit balance that reduces the recorded face value of the note to the actual amount received.

How do you record purchases with discounts?

Accounting for Early Pay Discounts: Gross Method When you pay the invoice, debit accounts payable for the total amount, credit your purchases discount account for the amount of the discount and credit cash for the difference between the invoice and the discount, explains Corporate Finance Institute.

What is a discount on a notes payable?

A discount on notes payable arises when the amount paid for a note by investors is less than its face value. The difference between the two values is the amount of the discount. This difference is gradually amortized over the remaining life of the note, so that the difference is eliminated as of the maturity date.

Are purchase discounts an expense?

Companies that take advantage of sales discounts usually record them in an account named purchases discounts, which is another contra‐expense account that is subtracted from purchases on the income statement.

How do you get discounts on notes receivable?

A five-step process is used in accounting for a discount on notes receivable:

- Compute the maturity value.

- Compute the discount (discount rate times maturity value).

- Compute the proceeds (maturity value less discount).

- Compute the net interest income or expense (proceeds less carrying value).

- Prepare the journal entry.

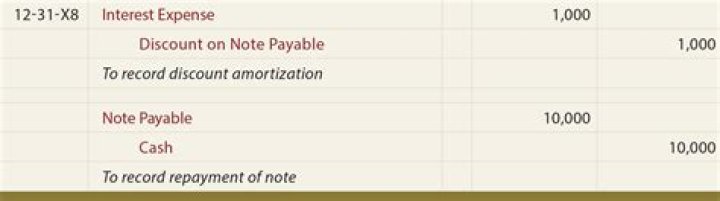

Is discount on notes payable an expense?

The discount on a notes payable account is a contra liability account. It follows the note payable, amortized over the five-year life. The process of amortization moves the discount balance (in the balance sheet) to the income statement via interest expense by using the effective interest method.

What does it mean to discount notes receivable?

Discounting Notes Receivable Just as accounts receivable can be factored, notes can be converted into cash by selling them to a financial institution at a discount. Notes are usually sold (discounted) with recourse, which means the company discounting the note agrees to pay the financial institution if the maker dishonors the note.

Do you have to record cash discount on purchase?

However, not all purchases may qualify for the cash discount. It is therefore necessary to record the initial purchase at the gross amount (after deducting any trade discounts though!) and subsequently decreasing purchases by the amount of discount that is actually received.

How are cash discounts recorded on a balance sheet?

Following double entry is required to record the cash discount: Crediting discount received has the effect of reducing gross purchases by the amount of cash discount received. Consequently, payables are debited to reduce their balance to the amount that is expected to be paid to them, i.e. net of cash discount.

How are trade discounts recorded in an accounting?

Trade discounts are generally ignored for accounting purposes in that they are omitted from accounting records. Therefore, purchases, along with any payables in the case of a credit purchase, are recorded net of any trade discounts offered.