How do I stop 10 percent penalty on IRA withdrawal?

One option for taking early distributions from a traditional IRA or for taking non-qualified Roth IRA distributions is to use the IRS’s section 72(t)(2) rule, which allows retirement account holders to avoid paying the 10 percent penalty by taking a series of substantially equal periodic payments (SEPPs) for five years …

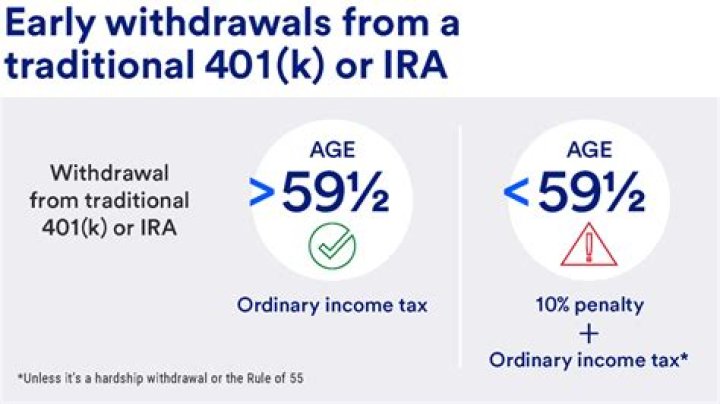

What is the 10 percent penalty on early withdrawal?

You may be subject to a 10% tax penalty for early withdrawal, in addition to any federal and state income tax on the withdrawal. The IRS charges a 10% penalty on withdrawals from qualified retirement plans before you reach age 59 ½, with certain exceptions.

What’s the penalty for early withdrawal from an IRA?

Generally, early withdrawal from an Individual Retirement Account (IRA) prior to age 59½ is subject to being included in gross income plus a 10 percent additional tax penalty. There are exceptions to the 10 percent penalty, such as using IRA funds to pay your medical insurance premium after a job loss.

What’s the penalty for cashing out my retirement account early?

If you cash out your retirement savings early, you may have to pay a penalty. Here’s how to figure out yours. The early withdrawal penalty and its exceptions In general, if you make a withdrawal from your retirement accounts before you reach age 59 1/2, the IRS will assess a 10% early withdrawal penalty.

What’s the penalty for taking money out of a Roth IRA?

If you withdraw Roth IRA earnings before age 59½, a 10% penalty usually applies. Withdrawals before age 59½ from a traditional IRA trigger a 10% penalty tax, whether you withdraw contributions or earnings. In certain IRS-approved situations, you may take early withdrawals from an IRA with no penalty.

Do you have to pay early distribution penalty on inherited IRA?

If you are the beneficiary of a deceased person’s IRA, amounts you distribute from the inherited IRA are not subjected to early-distribution penalties. This exception does not apply if you are the spouse-beneficiary of the decedent and decide to transfer or roll over the amount to your own non-inherited IRA.