How do you account for change from LIFO to FIFO?

Convert LIFO to FIFO statement

- Add the LIFO reserve to LIFO inventory.

- Deduct the excess cash saved from lower taxes under LIFO (i.e. LIFO Reserve x Tax rate)

- Increase the retained earnings component of shareholders’ equity by the LIFO reserve x (1-T)

- In the income statement, FIFO COGS = LIFO COGS – Δ LIFO Reserve.

When can you change from LIFO to FIFO?

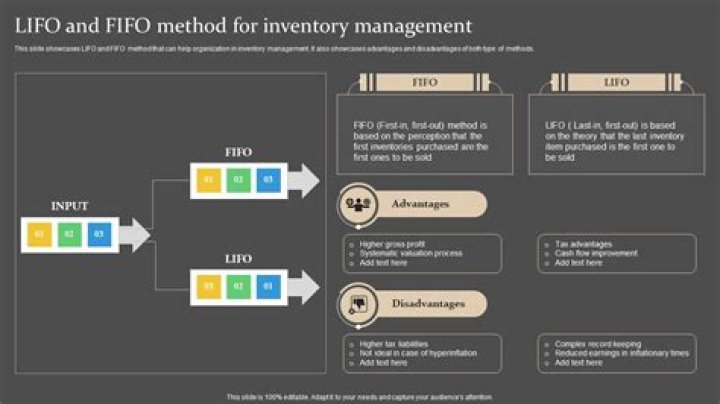

LIFO moves the latest/more recent costs from inventory and reports them as the cost of goods sold and leaves the first/oldest costs in inventory. A U.S. company may switch from FIFO to LIFO. However, after the switch the company must use LIFO consistently.

Is a change from LIFO to FIFO a change in accounting principle?

A change in accounting principles is a change in a method used, such as using a different depreciation method or switching between LIFO (Last In, First Out) to FIFO (First In, First Out) inventory valuation methods.

How can financial statements be converted from the LIFO basis to the FIFO basis of inventory valuation and vice versa?

The amount reported in the LIFOreserve can be used to convert the inventory valuation from LIFO to FIFO on the balance sheet. Inventoryvalued under the FIFO basis may be computed by adding the LIFO reserve to the LIFOending inventory on the balance sheet.

Can you switch from FIFO to LIFO?

If you plan on changing from FIFO to LIFO for tax purposes, you are required to complete Form 970 and comply with all requirements listed in the form. You must file the form with the return for the first tax year you plan on using LIFO.

Why would a company change from FIFO to LIFO?

Many companies use LIFO primarily because it allows lower income reporting for tax purposes. A change from LIFO to FIFO typically would increase inventory and, for both tax and financial reporting purposes, income for the year or years the adjustment is made.

Add the value of the LIFO reserve to the value of the inventory calculated by LIFO. The total will be the value of inventory if you use FIFO. To calculate the FIFO cost of goods sold, take the LIFO cost of goods sold and subtract the change in the LIFO reserve, which you already identified.

When can you switch from LIFO to FIFO?

Most companies switching from LIFO to FIFO choose to restate their historical financial statements as if the new method had been used all along. The income statement is affected from changes in cost of goods sold, and this affects all measures of earnings, such as operating income and net income.

Would you approve the proposal to move from LIFO to FIFO?

So yes I would absolutely approve this proposal to move from LIFO to FIFO. All because of the profits and bonuses that the company will come into after the big approval of the proposal. Everyone wins the company makes a bigger profit and the executives get bigger bonuses.

Why would a company change from LIFO to FIFO?

What happens when you switch from LIFO to FIFO?

How is the value of a LIFO reserve calculated?

How is LIFO reported on the income statement?

If the LIFO reserve decreases during a reporting period, the decrease in the reserve should be added to the cost of sales amount which is reported on the income statement. If a company uses the LIFO method, in converting the reported inventory amount to FIFO, the company has to: A. Add the disclosed LIFO reserve to the inventory balance.

What’s the difference between FIFO and last in first out?

However, in the case of inventory, companies have the freedom to choose between two accounting methods: first-in-first-out, or FIFO, and last-in-first-out, or LIFO. The decision can have a significant impact on a company’s reported earnings. While most companies stick with FIFO or LIFO for consistency, sometimes the owners change their minds.