How do you account for liquidation of a partnership?

Accounting for the liquidation of a partnership involves four steps as follows:

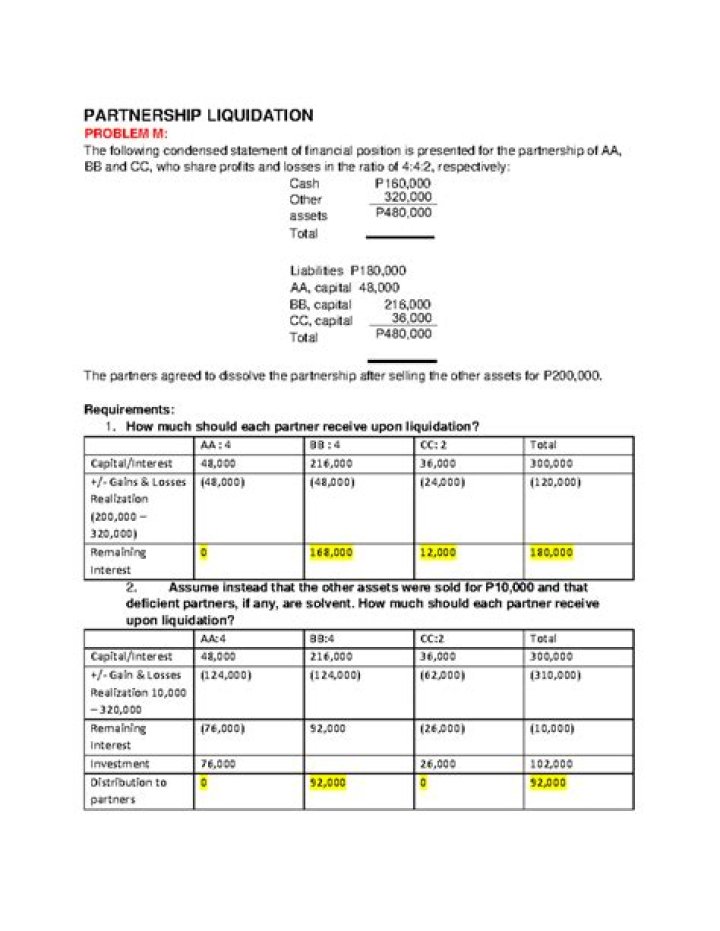

- Sell non cash assets for cash.

- Allocate any gain or loss on the sale of non cash assets to each partner using the income ratio.

- Pay any liabilities of the partnership.

- Distribute the remaining cash to the partners using the capital ratio.

What is the order of preference in the liquidation of a partnership?

Generally, however, the liquidators of a partnership pay non-partner creditors first, followed by partners who are also creditors of the partnership. If any assets remain after satisfying these obligations, then partners who have contributed capital to the partnership are entitled to their capital contributions.

What are the two types of liquidation in partnership accounting?

Types of LiquidationLUMP SUM LIQUIDATION – no distributions are made to partners until the realization process is completed when the full amount of realization gain or loss is known. INSTALLMENT LIQUIDATION – distributions are made to some or all of the partners as becomes available.

What are the possible causes for the liquidation of a partnership?

Partnership liquidation may be caused by any of the following: (1) accomplishment of the purpose of the partnership (2) termination of the term/ period covered by the partnership contract (3) bankruptcy of the partnership (4) mutual agreement among the partners to close the business.

What are the liabilities of the partnership in the order of payment?

The liabilities of the partnership shall rank in order of payment, as follows:

- Those owing to creditors other than partners,

- Those owing to partners other than for capital and profits,

- Those owing to partners in respect of capital,

- Those owing to partners in respect of profits.

Does a partnership dissolve when a partner dies?

A two-person partnership does not terminate upon a partner’s death if the deceased partner’s successor in interest (usually the estate) continues to share in the partnership’s profits or losses (Regs.

When does the sale of a partnership result in a single partner?

Based on the holding in McCauslen, 45 T.C. 588 (1966), and Rev. Ruls. 67 – 65 and 99 – 6, when a partnership terminates because a sale of partnership interests results in a single partner, the selling partner follows the normal rules for recognizing gain or loss on the sale of the partnership interest.

Can a partnership buy out an exiting partner?

The federal income tax rules for partnership payments to buy out an exiting partner’s interest are tricky, but they also open up tax planning opportunities. Payments made by a partnership to liquidate (or buy out) an exiting partner’s entire interest are covered by Section 736 of the Internal Revenue Code.

What happens when a partner leaves a partnership?

For withdrawal of a partnership, either from death or choice, there are a several scenarios: The individual partners pay, with their own cash and not the partnership cash, the leaving partner for a share of the leaving partner’s capital account. The partnership pays the leaving partner for the value of his or her capital account + a cash bonus.

How is a partner added to a partnership?

The journal entry to withdrawal of S. Leavy from the partnership is: A partner can be added to an existing partnership in four ways, including: New partner can purchase part of the interest of another partner. New partner can invest cash or other assets in the business.