How do you analyze a Statement of Changes in Equity?

Statement of Changes in Equity is the reconciliation between the opening balance and closing balance of shareholder’s equity. It is a financial statement which summarises the transactions related to the shareholder’s equity over an accounting period.

How do you find changes in equity?

Retained Earnings are part of the “Statement of Changes in Equity”. The general equation can be expressed as following: Ending Retained Earnings = Beginning Retained Earnings − Dividends Paid + Net Income.

What is an unexplained adjustment to retained earnings?

It represents the amount of money you have to reinvest in your business or distribute to shareholders through dividend payments. An unexplained adjustment to retained earnings is an accounting method to reconcile changes that are not represented your periodic income statement.

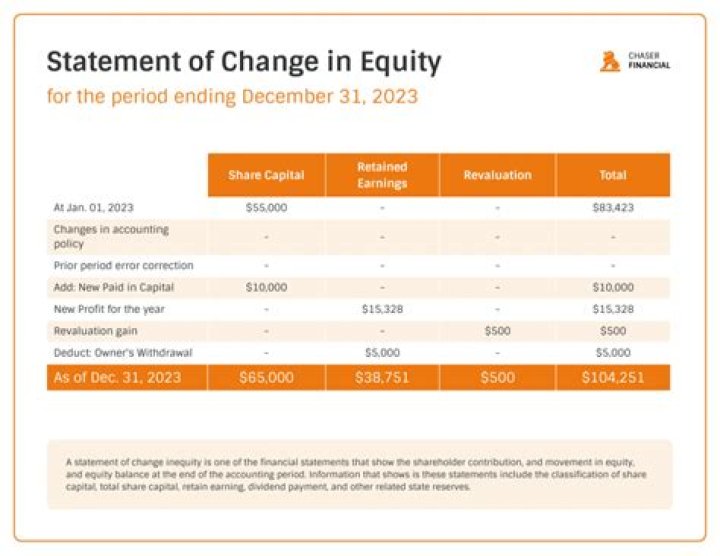

What information can we get from a Statement of Changes in Equity?

6.2 The statement of changes in equity presents an entity’s profit or loss for a reporting period, items of income and expense recognised in other comprehensive income for the period, the effects of changes in accounting policies and corrections of errors recognised in the period, and the amounts of investments by, and …

How do you prepare a statement of change in equity?

How to Prepare a Statement of Changes in Equity

- Step 1: Collect the Needed Information. The first step to creating the statement is to gather information from the adjusted trial balance.

- Step 2: Title the Statement.

- Step 3: Beginning Balances.

- Step 4: Additions.

- Step 5: Deductions.

- Step 6: Ending Balances.

Who uses the statement of changes in equity?

Statement of changes in equity delivers the consumers with financial data for three main elements of equity, comprising: A settlement among the amount during the start and the closing of the period of a respective factor of equity, like retained earnings, share capital, and revision.

Do I need a statement of changes in equity?

Note that the statement must be clearly shown as a statement of income and retained earnings. It is the composite nature of the statement which needs to be clear. If, in future years, there are other changes and a separate statement of comprehensive income and statement of changes in equity are required, so be it.

What causes increase or decrease in equity?

The cash proceeds, less any expenses related to the offering, boost the company’s assets and in turn create an increase in stockholders’ capital as well. The other primary way that stockholders’ equity changes is when the business makes a profit. However, it’s not enough that the company make money.

What causes a decrease in owner’s equity?

Owner’s equity decreases if you have expenses and losses. If your liabilities become greater than your assets, you will have a negative owner’s equity. You can increase negative or low equity by securing more investments in your business or increasing profits.