How do you calculate book value per share?

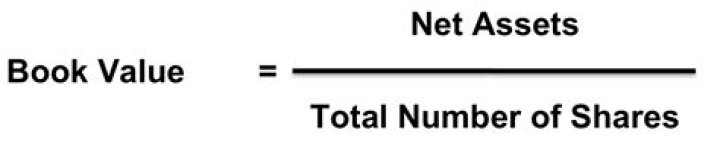

Book value per share is calculated by totaling the company’s assets, subtracting all debt, liabilities, and the liquidation price of preferred stock, then dividing the result by the number of outstanding shares of common stock.

Is revaluation surplus part of equity?

A revaluation surplus is an equity account in which is stored any upward changes in the value of capital assets. If a revalued asset is subsequently dispositioned out of a business, any remaining revaluation surplus is credited to the retained earnings account of the entity.

How do you calculate book value per share in the Philippines?

If there are both common and preferred shares, the book value per common share is computed by deducting the liquidation value of the preferred shares from the total equity of the corporation and dividing the result by the number of outstanding common shares as of balance sheet date nearest to the transaction date.

What is included in book value?

Book value is the accounting value of the company’s assets less all claims senior to common equity (such as the company’s liabilities). The term book value derives from the accounting practice of recording asset value at the original historical cost in the books.

What is the treatment of revaluation surplus?

Revaluation Surplus The asset account is debited (increased) for the increase in value or credited (decreased) for a decrease in value.

How do you solve revaluation surplus?

Revaluation Surplus Formula

- Revaluation Surplus can be calculated by the following simple formula.

- Revaluation Surplus = Revalued Amount – Net book Value.

- Plant Cost = 100,000.

- Net book value = 80,000.

- Revalued amount= 120,000.

- What would be revaluation Surplus?

- Revaluation Surplus = Revalued amount- net book value.

What if book value is more than share price?

When compared to the current market value per share, the book value per share can provide information on how a company’s stock is valued. If the value of BVPS exceeds the market value per share, the company’s stock is deemed undervalued. For example, if a company shows an intrinsic value of $11.

Is a higher book value better?

Market Value Greater Than Book Value It indicates that investors believe the company has excellent future prospects for growth, expansion, and increased profits. They may also think the company’s value is higher than what the current book valuation calculation shows.

How is revaluation calculated?

Definition and explanation. Under revaluation method a competent person values the asset concerned at the end of each financial year and the depreciation is calculated by deducting the value at the end of the year from the value at the beginning of the year.

Is a high book value per share good?

Understanding Book Value Per Share (BVPS) If a company’s BVPS is higher than its market value per share—its current stock price—then the stock is considered undervalued. If the firm’s BVPS increases, the stock should be perceived as more valuable, and the stock price should increase.

What does a high price book value mean?

A High Price-to-Book (P/B) Ratio A P/B ratio that’s greater than one suggests that the stock price is trading at a premium to the company’s book value. For example, if a company has a price-to-book value of three, it means that its stock is trading at three times its book value.

How do you calculate adjusted book value per share?

The goal is to mark each asset and liability to fair market value. After the values of all the assets and liabilities are adjusted, the analyst must simply deduct the liabilities from the assets to derive the fair value of the firm.

Is a high book value per share good or bad?

2 Answers. The book value per share is the amount of the assets that will go to common equity in the event of liquidation. So higher book value means the shares have more liquidation value. Strictly speaking, the higher the book value, the more the share is worth.

What is a good book value per share?

Updated Apr 26, 2021. The price-to-book (P/B) ratio has been favored by value investors for decades and is widely used by market analysts. Traditionally, any value under 1.0 is considered a good P/B value, indicating a potentially undervalued stock.

How is revaluation surplus treated?

A revaluation loss should be charged against any related revaluation surplus to the extent that the decrease does not exceed the amount held in the revaluation surplus in respect of the same asset. Any additional loss must be charged as an expense in the statement of profit or loss.

How do I book a revaluation surplus?

An increase in the asset’s value should not be reported on the income statement; instead an equity account is credited called “Revaluation Surplus. ” Revaluation surplus is reported in the other comprehensive income sub-section of the owner’s equity section in the balance sheet.

What does an increase in book value per share mean?

How does revaluation surplus affect the value of assets?

Revaluation surplus. In general, value of assets decrease over time but it may increase in certain circumstances especially in inflationary economies. Accounting standards allows two models for accounting of fixed assets.

How is impairment loss recorded on a revalued asset?

If a revalued asset is subsequently valued down due to impairment, the loss is first written off against any balance available in the revaluation surplus and if the loss exceeds the revaluation surplus balance of the same asset the difference is charged to income statement as impairment loss.

How is the carrying amount on revaluation calculated?

Calculation of carrying amount on revaluation date: Calculation of Revaluation Gain/reserve: Revaluation loss should be charged against any related revaluation surplus to the extent that the decrease does not exceed the amount held in the revaluation surplus in respect of the same asset.

How is upward revaluation recorded on the income statement?

It is recorded through the following journal entry: Upward revaluation is not considered a normal gain and is not recorded in income statement rather it is directly credited to a shareholders’ equity account called revaluation surplus. Revaluation surplus holds all the upward revaluations of a company’s assets until those assets are disposed of.