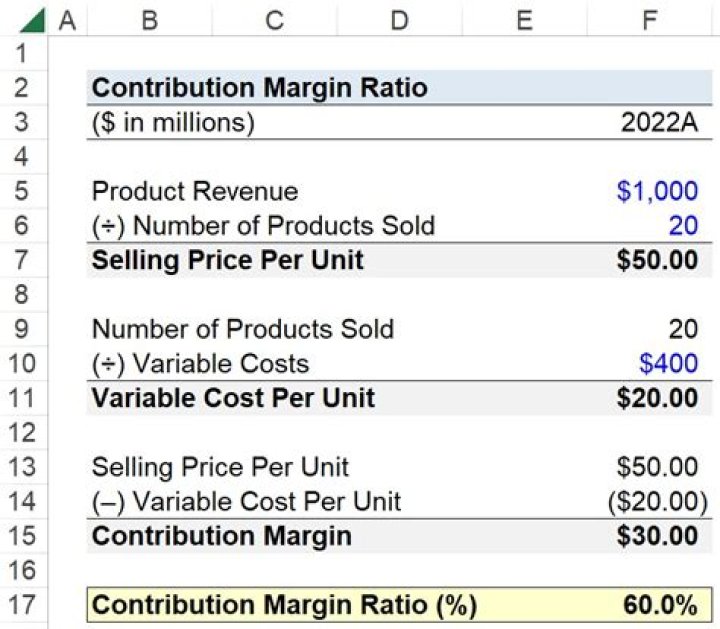

How do you calculate contribution margin ratio?

How to Calculate Contribution Margin

- Net Sales – Variable Costs = Contribution Margin.

- (Product Revenue – Product Variable Costs) / Units Sold = Contribution Margin Per Unit.

- Contribution Margin Per Unit / Sales Price Per Unit = Contribution Margin Ratio.

What is the contribution margin ratio example?

Working example: Contribution margins in a café Variable costs are all the direct costs that contribute to producing that delicious cup of coffee for the customer. Variable costs total $1,000. The contribution margin is $6,000 – $1,000 = $5,000. The contribution margin ratio shows a margin of 83% ($5,000/$6,000).

What is the CS ratio?

The C/S ratio (also confusingly known as the PV ratio) is normally expressed as a percentage. It is constant at all levels of activity. The C/S ratio reveals the amount of contribution that is earned for every $1 worth of sales revenue.

What does a high contribution margin ratio mean?

The closer a contribution margin percent, or ratio, is to 100%, the better. The higher the ratio, the more money is available to cover the business’s overhead expenses, or fixed costs. If the contribution margin is extremely low, there is likely not enough profit available to make it worth keeping.

Why is contribution margin ratio important?

This ratio shows the amount of money available to cover fixed costs. It is good to have a high contribution margin ratio, as the higher the ratio, the more money per product sold is available to cover all the other expenses.

How does CS calculate average ratio?

The weighted average C/S ratio of 0.34375 or 34.375% has been calculated by calculating the total contribution earned across both products and dividing that by the total revenue earned across both products.

What is contribution ratio?

The contribution margin ratio is the difference between a company’s sales and variable costs, expressed as a percentage. This ratio shows the amount of money available to cover fixed costs. This would increase the variable costs by $1 per unit, bringing the variable cost per unit to $5.

What is a positive contribution margin?

If a product has a positive contribution margin, it’s probably worth keeping. According to Knight, this is true even if the product’s “conventionally calculated profit is negative,” because “if the product has a positive contribution margin, it contributes to fixed costs and profit.”

Formula for Contribution Margin

- Contribution Margin = Net Sales Revenue – Variable Costs. OR.

- Contribution Margin = Fixed Costs + Net Income. To determine the ratio:

- Contribution Margin Ratio = (Net Sales Revenue -Variable Costs ) / (Sales Revenue) Sample Calculation of Contribution Margin.

What is contribution margin ratio used for?

The contribution margin ratio is the difference between a company’s sales and variable expenses, expressed as a percentage. In particular, it can be used to estimate the decline in profits if sales drop, and so is a standard tool in the formulation of budgets.

Is a higher contribution margin better?

The closer a contribution margin percent, or ratio, is to 100%, the better. The higher the ratio, the more money is available to cover the business’s overhead expenses, or fixed costs. Eliminating low contribution margin products can positively impact a company’s overall contribution margin.

What is difference between contribution margin and gross margin?

Gross margin is the amount of money left after subtracting direct costs, while contribution margin measures the profitability of individual products. Contribution margin can be used to examine variable production costs and is usually expressed as a percentage.

What is unit contribution margin?

The contribution margin is computed as the selling price per unit, minus the variable cost per unit. Also known as dollar contribution per unit, the measure indicates how a particular product contributes to the overall profit of the company.

What is the unit contribution margin?

What happens if contribution margin increases?

When you increase the contribution margin of the products you sell, you are decreasing the costs and expenses associated with each product and increasing the amount of revenue each product generates. The result of is a decrease in your break-even point.

How to calculate an overall contribution margin ratio?

Contribution margin ratio is calculated by dividing contribution margin figure by the net sales figure . The formula can be written as follows: The ratio is also shown in percentage form as follows:

What is the formula for calculating the contribution margin?

Calculation (formula) Contribution margin can be calculated by using the following formula: Contribution Margin = (Sale Revenue – Variable Costs) / Sales Revenue. The above formula calculates the contribution margin for all of the units sold.

How do you calculate total contribution margin?

To calculate the total contribution margin, start with the sales revenue generated by a product; this is the total amount you received from selling the product. From that amount, subtract the total variable costs in the production run. The result is the margin. For example, say you produced 105,000 shirts.

When does the Contribution Margin Ratio always increase?

The contribution margin ratio increases when sales increase. For every $1 increase in sales, profits increase by the contribution margin ratio. For example, if a company’s contribution margin ratio is 25 percent, it is earning roughly 25 cents in profit for every one dollar in sales.