How do you calculate estimated bad debts?

Estimating your bad debts usually involves some form of the percentage of bad debt formula, which is just your past bad debts divided by your past credit sales. Let’s say you’ve been in business for a year, and that of the total $300,000 in credit sales you made in your first year, $20,000 ended up uncollectable.

What are the two methods of accounting for bad debts which is in accordance with GAAP?

There are two ways to record a bad debt, which are: Direct write-off method. If you only reduce accounts receivable when there is a specific, recognizable bad debt, then debit the Bad Debt expense for the amount of the write off, and credit the accounts receivable asset account for the same amount. Allowance method.

What is the estimate of bad debt expense?

Alternatively, a bad debt expense can be estimated by taking a percentage of net sales, based on the company’s historical experience with bad debt. Companies regularly make changes to the allowance for credit losses entry, so that they correspond with the current statistical modeling allowances.

How is bad debt accounted for in GAAP?

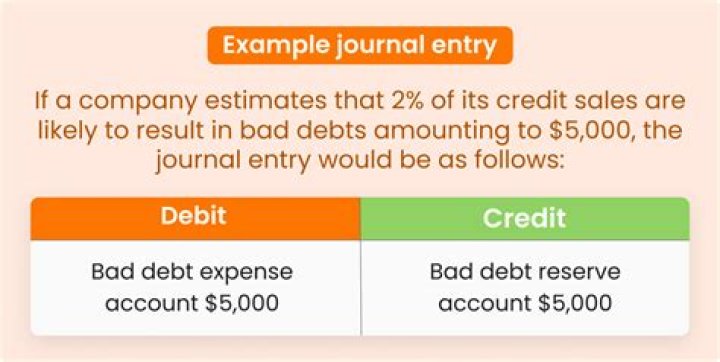

Because it is impossible to know precisely which accounts will turn bad, there are three GAAP procedures for estimating (forecasting) the allowance for bad debt: the percentage of credit sales method, the aging of accounts receivable method (a variation of the preceding) and the percentage of ending accounts receivable method.

How do companies estimate the value of bad debts?

One way companies derive an estimate for the value of bad debts under the allowance method is to calculate bad debts as a percentage of the accounts receivable balance. If a company has $100,000 in accounts receivable at the end of an accounting period and company records indicate that, on average,…

How are bad debt expenses calculated in a general ledger?

Under the allowance method of calculating bad debts, there are two general ledger accounts – bad debts, an expense account, and allowance for doubtful accounts, a contra-asset account used to offset to the accounts receivable balance. To record the bad debt expenses, you must debit bad debt expense and a credit allowance for doubtful accounts.

How is the entry for bad debts adjusted?

Companies that use the percentage of credit sales method base the adjusting entry solely on total credit sales and ignore any existing balance in the allowance for bad debts account. If estimates fail to match actual bad debts, the percentage rate used to estimate bad debts is adjusted on future estimates.