How do you calculate expected return standard deviation and coefficient of variation?

How to calculate coefficient of variation

- Determine volatility. To find volatility or standard deviation, subtract the mean price for the period from each price point.

- Determine expected return. To find the expected return, multiply potential outcomes or returns by their chances of occurring.

- Divide.

- Multiply by 100%

How do you find covariance with standard deviation and expected return?

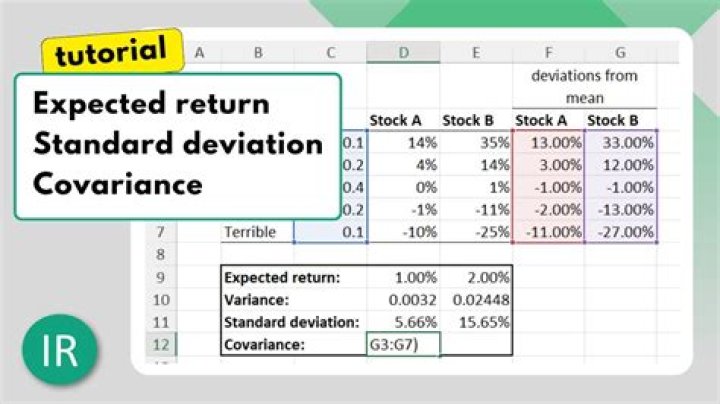

Covariance is calculated by analyzing at-return surprises (standard deviations from the expected return) or by multiplying the correlation between the two variables by the standard deviation of each variable.

How do you find the coefficient of standard deviation?

σ is the standard deviation for a population, which is the same as “s” for the sample. μ is the mean for the population, which is the same as XBar in the sample. In other words, to find the coefficient of variation, divide the standard deviation by the mean and multiply by 100.

Is it better to have a higher or lower coefficient of variation?

The higher the coefficient of variation, the greater the level of dispersion around the mean. It is generally expressed as a percentage. The lower the value of the coefficient of variation, the more precise the estimate.

How do you interpret standard deviation and coefficient of variation?

If you know nothing about the data other than the mean, one way to interpret the relative magnitude of the standard deviation is to divide it by the mean. This is called the coefficient of variation. For example, if the mean is 80 and standard deviation is 12, the cv = 12/80 = . 15 or 15%.

What is the difference between correlation and covariance?

“Covariance” indicates the direction of the linear relationship between variables. “Correlation” on the other hand measures both the strength and direction of the linear relationship between two variables. Correlation is a function of the covariance.

What’s the difference between expected return and standard deviation?

A: Expected return and standard deviation are two statistical measures that can be used to analyze a portfolio. The expected return of a portfolio is the anticipated amount of returns that a portfolio may generate, whereas the standard deviation of a portfolio measures the amount that the returns deviate from its mean.

How to calculate the coefficient of standard deviation?

Calculate the coefficient of standard deviation and coefficient of variation from the following distribution of marks: Coefficient of Standard Deviation = S X ¯ = 2 4 = 0.5

How is the standard deviation of a portfolio calculated?

Conversely, the standard deviation of a portfolio measures how much the investment returns deviate from the mean of the probability distribution of investments. The standard deviation of a two-asset portfolio is calculated as: σ P = √ ( w A2 * σ A2 + w B2 * σ B2 + 2 * w A * w B * σ A * σ B * ρ AB )

How to calculate portfolio expected return and variance?

Portfolio expected return and variance For the sake of simplicity, we will construct a portfolio with only two risky assets. The portfolio’s expected return is a weighted average of its individual assets’ expected returns, and is calculated as: E (Rp) = w1E (R1) + w2E (R2)