How do you calculate lost contribution margin?

Lost Contribution Breakdown Take the previous description of investment Decision B and its $150,000 lost contribution margin. You could break this down to lost contribution margin per unit by taking the $150,000 and dividing it by 15,000 units produced. This equals a lost contribution margin per unit of $10.

Does contribution margin include cogs?

An alternative to the gross margin concept is contribution margin, which is revenues minus all variable costs of sales. By excluding all fixed costs, the content of the cost of goods sold figure now changes to the following: Direct materials.

What is the difference between margin and contribution margin?

Gross profit margin measures the amount of revenue that remains after subtracting costs directly associated with production. Contribution margin is a measure of the profitability of various individual products.

How to calculate contribution margin for a business?

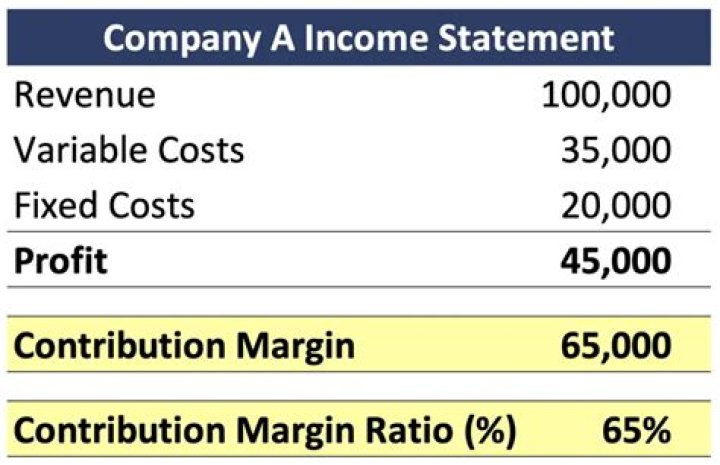

Formula for Contribution Margin. In terms of computing the amount: Contribution Margin = Net Sales Revenue – Variable Costs. OR. Contribution Margin = Fixed Costs + Net Income. To determine the ratio: Contribution Margin Ratio = (Net Sales Revenue -Variable Costs ) / (Sales Revenue) Sample Calculation of Contribution Margin

Which is the unit contribution margin per unit?

Unit contribution margin per unit denotes the profit potential of a product or activity from the sale of each unit to cover per unit fixed cost and generate profit for the firm. E.g. a firm sales a product at Rs 10 per piece and incurred variable costs per unit Rs 7, the unit contribution margin will be Rs 3 (10 – 7).

What do you mean by low contribution margin?

Low or negative contribution margin Contribution Margin Contribution margin is a business’ sales revenue less its variable costs. The resulting contribution margin can be used to cover its fixed costs (such as rent), and once those are covered, any excess is considered earnings.

Why is contribution margin important in break even analysis?

Key Takeaways. The contribution margin represents the portion of a product’s sales revenue that isn’t used up by variable costs, and so contributes to covering the company’s fixed costs. The concept of contribution margin is one of the fundamental keys in break-even analysis.