How do you calculate standard deviation from risk and return?

To find standard deviation on a mutual fund, add up the rates of return for the period you want to measure and divide by the total number of rate data points to find the average return. Further, take each individual data point and subtract your average to find the difference between reality and the average.

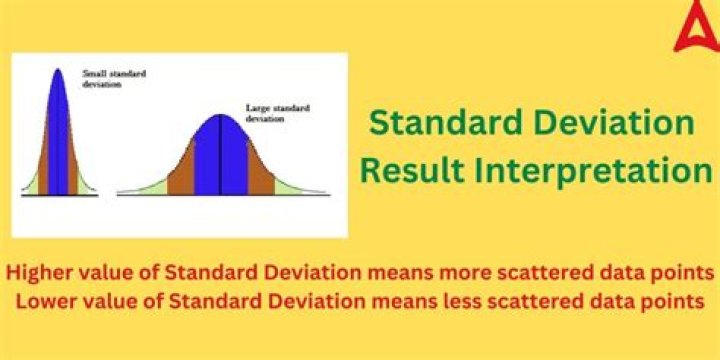

What is acceptable standard deviation?

For an approximate answer, please estimate your coefficient of variation (CV=standard deviation / mean). As a rule of thumb, a CV >= 1 indicates a relatively high variation, while a CV < 1 can be considered low. A “good” SD depends if you expect your distribution to be centered or spread out around the mean.

What’s the difference between expected return and standard deviation?

A: Expected return and standard deviation are two statistical measures that can be used to analyze a portfolio. The expected return of a portfolio is the anticipated amount of returns that a portfolio may generate, whereas the standard deviation of a portfolio measures the amount that the returns deviate from its mean.

How is the standard deviation of a portfolio calculated?

Conversely, the standard deviation of a portfolio measures how much the investment returns deviate from the mean of the probability distribution of investments. The standard deviation of a two-asset portfolio is calculated as: σ P = √ ( w A2 * σ A2 + w B2 * σ B2 + 2 * w A * w B * σ A * σ B * ρ AB )

How is the expected return of a portfolio calculated?

The expected return of a portfolio is calculated by multiplying the weight of each asset by its expected return and adding the values for each investment. For example, a portfolio has three investments with weights of 35% in asset A, 25% in asset B, and 40% in asset C.

What is the expected return of an asset?

The expected return of asset A is 6%, the expected return of asset B is 7%, and the expected return of asset C is 10%. [ (35% * 6%) + (25% * 7%) + (40% * 10%)] = 7.85% This is commonly seen with hedge fund and mutual fund managers, whose performance on a particular stock isn’t as important as their overall return for their portfolio.