How do you format a cash flow statement?

The cash flow statement follows an activity format and is divided into three sections: operating, investing and financing activities. Generally, the operating activities are reported first, followed by the investing and finally, the financing activities.

How do you calculate net cash flow using the indirect method?

With the indirect method, cash flow is calculated by taking the value of the net income (i.e. net profit) at the end of the reporting period. You then adjust this net income value based on figures within the balance sheet and strip-out the effect of non-cash movements shown on the profit and loss statement.

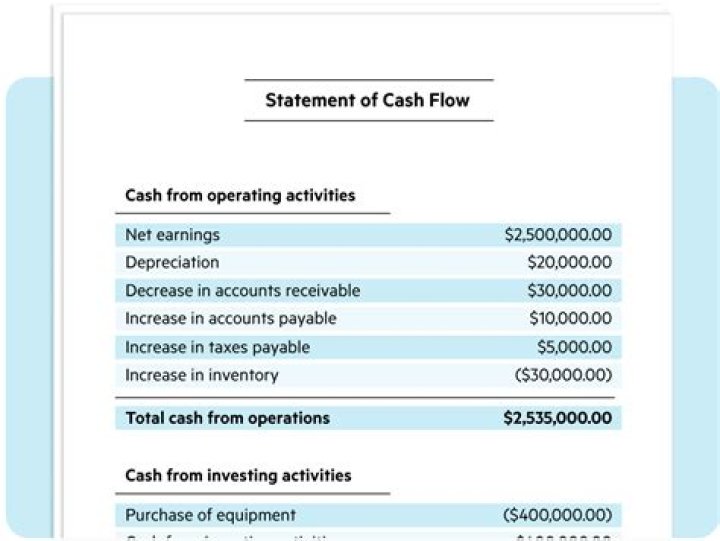

How to prepare an indirect method cash flow statement?

Let’s take a look at the format and how to prepare an indirect method cash flow statement. Format The indirect operating activities section always starts out with the net income for the period followed by non-cash expenses, gains, and losses that need to be added back to or subtracted from net income .

How can I make my own cash flow statement?

View on YouTube! This template enables users to automatically compile a complete cash flow statement by simply entering basic income statement and balance sheet information. The template includes a current and comparative financial period and detailed instructions on the calculation of the line items which are included on the cash flow statement.

How are non cash items included in a cash flow statement?

The calculation starts with the profit or loss before taxation and all non-cash income & expenses and items which are included in other line items on the cash flow statements are then added back from the calculated amounts. Investment income and interest expenses are added back because these items are included separately on the cash flow statement.

Why do I need to Subtract income from cash flow statement?

Thus, a net increase in an asset account actually decreased cash, so we need to subtract this increase from the net income. The opposite is true about decreases. If an asset account decreases, we will need to add this amount back into the income. Here’s a general rule of thumb when preparing an indirect cash flow statement: