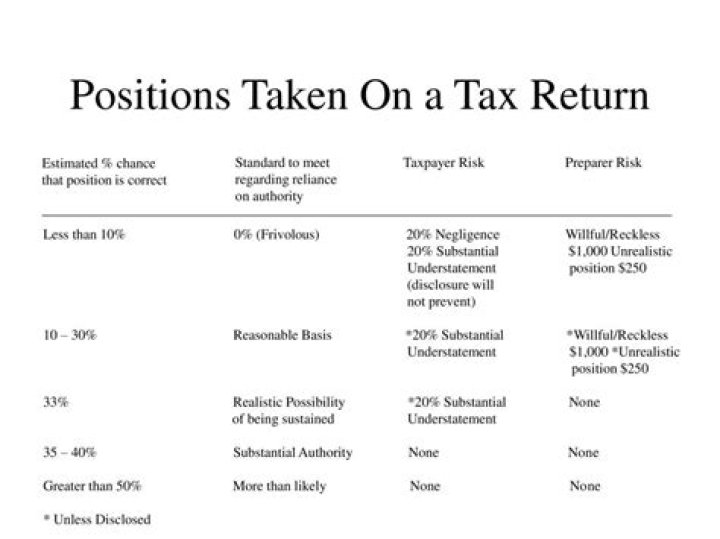

How do you know when there is substantial authority for a tax return position?

Under IRS rules, the tax treatment of an item has “substantial authority” only if the weight of published cases, rules and other legal and administrative authorities is substantial in relation to the weight of opposing authorities.

Can you go to jail for lying on taxes?

“Tax fraud is a felony and punishable by up to five years in prison,” said Zimmelman. “Failing to report foreign bank and financial accounts might result in up to 10 years in prison.” Courts convict approximately 3,000 people every year of tax fraud, signaling how serious the IRS takes lying on your taxes.

Should a tax opinion?

A “should” opinion” suggests a reasonably high level of confidence that the position will be sustained— significantly higher than “more likely than not”—but allows for a not insignificant risk of being wrong. Will Opinion. A “will” opinion is consistent with a conclusion that there is no material risk of being wrong.

Does a tax position always have to meet at minimum the substantial authority standard?

In summary, under IRC section 6662(d), taxpayers must have substantial authority that is higher than a reasonable-basis threshold, but less than the more-likely-than-not threshold to take a position on a tax return without disclosure.

How to ask a tax expert for answers?

Ask a Tax Expert for Answers ASAP Experts are full of valuable knowledge and are ready to help with any question. Credentials confirmed by a Fortune 500 verification firm. Via email, text message, or notification as you wait on our site. Ask follow up questions if you need to. Rate the answer you receive. Ask Tax Questions Online.

Where can I get the best tax advice?

From questions regarding tax advice, deductions and credits, dependents, exemptions, filing status, audits, disputes, tax payer rights and more. Tax Experts on JustAnswer can give you all the tax advice you need at an affordable cost. Type Your Tax Question Here…

Which is more likely than not in SEC 6662a?

“More likely than not” (which is the standard that applies to a tax shelter or a reportable transaction to which Sec. 6662A applies) is defined as being of the reasonable belief that the position would more likely than not be sustained on its merits (Sec. 6694 (a) (2) (C)), i.e., at least a bit more than 50% chance of success based on its merits.

How are substantial authority and reasonable basis defined?

Both substantial authority and reasonable basis are essentially defined as a conceptual level of confidence; that is, as a determined weight of authorities that support the desired tax treatment of the facts of the situation, out of the total weight of authorities that address the facts of the situation (Regs. Secs.