How do you make a ledger trial balance?

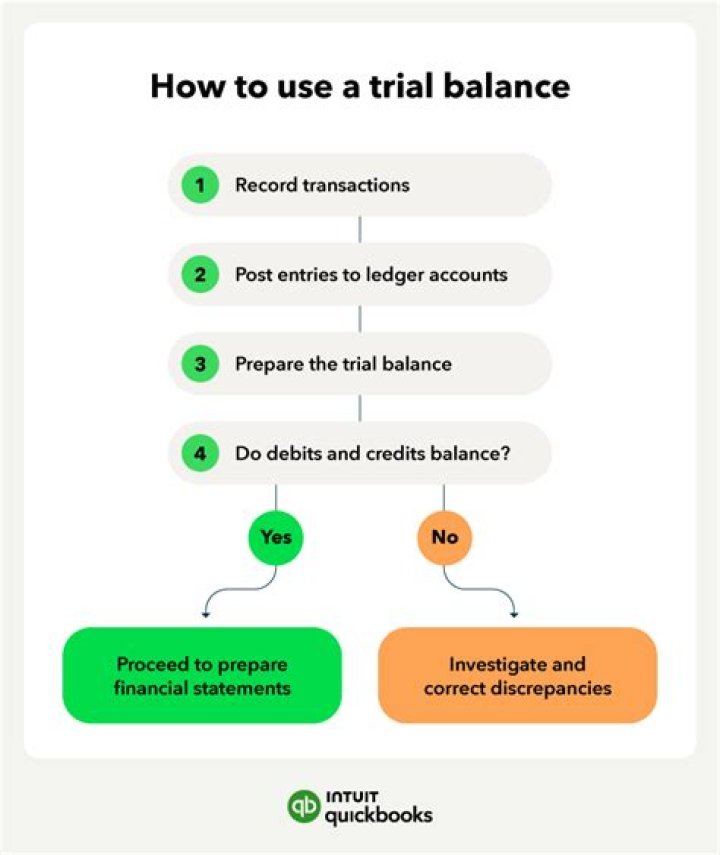

In order to prepare a trial balance at any time, it is necessary to determine the balance on each account. This process is known as ‘balancing off’ the general ledger accounts. The trial balance can then be prepared by listing each closing balance from the general ledger accounts as either a debit or a credit balance.

How is balance brought forward calculated?

Calculate the discrepancy between the large side and the small side (5,370-400=4,970) and set the figure in the small side naming it to balance carried forward (c/f). In this case, it’s the credit; The balance b/f is inserted to the debit column just below the totals line.

How do you balance off an account?

Balancing off Accounts Process

- Total both the debit and credit sides of the ledger account.

- Calculate the balance (the difference between the total debits and total credits)

- Add a one sided entry to make the totals on both sides of the account equal.

How often are ledger accounts balanced?

A ledger balance is computed by a bank at the end of each business day and includes all withdrawals and deposits to calculate the total amount of money in a bank account. The ledger balance is the opening balance in the bank account the next morning and remains the same all day.

How do you fix an out of balance general ledger?

Tips and Tricks: How To Correct Unbalanced General Ledger

- Click File, Print Reports, General Ledger.

- Double click Trial balance.

- Fiscal period ending should default with current month end date.

- Leave Report consolidation unchecked.

- Click OK.

What is the difference between ledger and trial balance?

The general ledger contains the detailed transactions comprising all accounts, while the trial balance only contains the ending balance in each of those accounts. They use the general ledger for a different purpose, which is to trace balances back to individual transactions.

What is the difference between carry forward and brought forward?

Brought forward means balance which was brought froward from Previous month or year. and carry forward is to carry the balance in next year.

What is the difference between balance brought down and carried down?

Balance brought down is the opening balance of a ledger account that is brought into the books from a previous accounting period. Balance carried down is the closing balance of a ledger account that is carried forward to the next accounting period.

What is out of balance journal entries?

An out of balance Journal Entry is created (debits do not equal credits) after a batch is created from posting a bill with negative allocations (positive and negative fees/expenses) and prepaid applied. For additional details, see Applying Prepaid Funds to an A/R Balance for Previous Bills.

What is balance brought forward and balance carried forward?

Definition: the balance brought forward vs the balance carried forward. Brought forward – the balance at the beginning of the period. Carried forward – the balance at the end of the period. Formula: cash balance carried forward.

In short, a ledger is an account wise summary of all monetary transactions, whereas a trial balance is the debit and credit balance of such ledger accounts. Traditionally a ledger was prepared in a physical book with a separate page for each account and a trial balance was derived from these accounts.

What is the balance off rule?

Balancing off means matching figures of debits and credits of the account.

How to balance a ledger with debit and credit?

Folioing – Put the page number for a journal entry on the ledger account’s folio column. Casting – Separating debit and credit amount. Balancing – find the difference between debit and credit to get debit or credit balance of the account. 1. Drawing the Form – Get pen and paper, Start Drawing the Ledger Account.

Where does balance B / F Go in ledger account?

The balance b/f is inserted to the debit column just below the totals line. This is going to be the closing balance for that particular period. As we mentioned in the beginning, for the ledger account to have a credit balance, the amount of the credits must be greater than the debit figure.

What does balancing of Ledger mean in accounting?

At the end of every accounting year all the accounts which are operated in the ledger book are closed, totaled and balanced. Balancing of ledgers means finding the difference between the debit and credit amounts of a particular account i.e. heavier total and lighter total difference and recording that difference amount on the lighter total side.

How is balance carried forward in a ledger?

The balance in the ledger has been recycled to the income statement which is being debited by the same amount. Unlike balance sheet ledger accounts, there is no balance brought down or carried forward. Instead, the income statement ledger is closed each accounting period end with the balancing figure representing the charge to income statement.