How do you measure portfolio performance?

Since you hold investments for different periods of time, the best way to compare their performance is by looking at their annualized percent return. For example, you had a $620 total return on a $2,000 investment over three years. So, your total return is 31 percent. Your annualized return is 9.42 percent.

What is the Sharpe measure for the portfolio?

Sharpe Ratio

The Sharpe Ratio is a financial metric often used by investors when assessing the performance of investment management products and professionals. It consists of taking the excess return of the portfolio, relative to the risk-free rate, and dividing it by the standard deviation of the portfolio’s excess returns.

Which is better Sharpe or Treynor?

While standard deviation measures the total risk of the portfolio, the Beta measures the systematic risk. Therefore, Sharpe is a good measure where the portfolio is not properly diversified while Treynor is a better measure where the portfolios are well diversified.

What is a good portfolio performance?

Generally speaking, if you’re estimating how much your stock-market investment will return over time, we suggest using an average annual return of 6% and understanding that you’ll experience down years as well as up years.

Is a higher Sharpe ratio good or bad?

A Sharpe ratio of 1.0 is considered acceptable. A Sharpe ratio of 2.0 is considered very good. A Sharpe ratio of 3.0 is considered excellent. A Sharpe ratio of less than 1.0 is considered to be poor.

Which is the best tool to measure portfolio performance?

Today, there are three sets of performance measurement tools to assist with portfolio evaluations. The Treynor, Sharpe, and Jensen ratios combine risk and return performance into a single value, but each is slightly different.

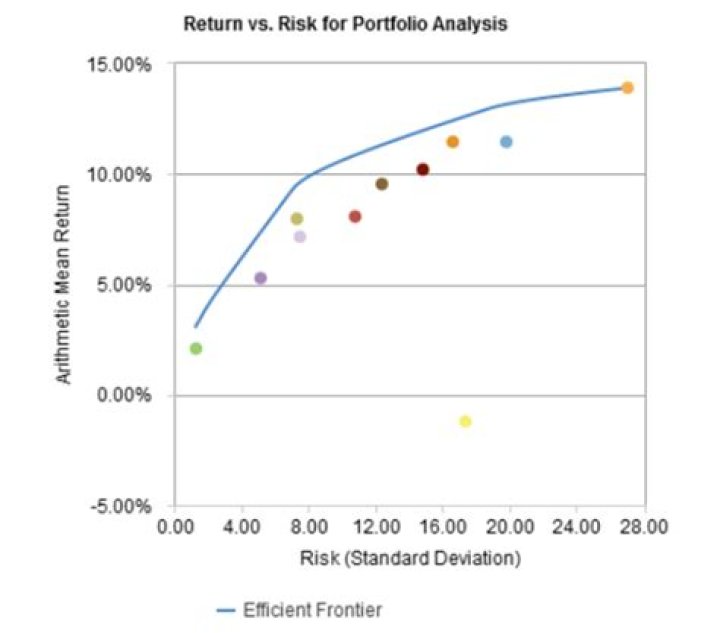

How do you measure risk in a portfolio?

If you measure risk by the standard deviation of the portfolio return σ = √wTΣw, then it is usual to define risk contributions for each asset by σi = wi(Σw)i/σ, then diversified could mean that these σi are evenly spread over the assets in the portfolio.

Which is the best way to rate a portfolio manager?

We’ll look at the five common ones in this article. The Sharpe ratio, also known as the reward-to-variability ratio, is perhaps the most common portfolio management metric. The excess return of the portfolio over the risk-free rate is standardized by the standard deviation of the excess of the portfolio return.

How is the Treynor ratio used to measure portfolio performance?

The Treynor ratio, also known as the reward-to-volatility ratio, is a performance metric for determining how much excess return was generated for each unit of risk taken on by a portfolio. The Sharpe ratio is used to help investors understand the return of an investment compared to its risk.