How do you record end of year depreciation?

Depreciation is recorded by debiting Depreciation Expense and crediting Accumulated Depreciation. This is recorded at the end of the period (usually, at the end of every month, quarter, or year). Depreciation Expense: An expense account; hence, it is presented in the income statement.

How do you close a depreciation expense?

Close out the Depreciation Expense account. Expense accounts are temporary, so they must be closed at the end of each accounting period. To do this move the $1,000 balance from the Depreciation Expense account into the Income Summary account. From there it will be moved into the Retained Earnings account.

Do I take depreciation in the year of sale?

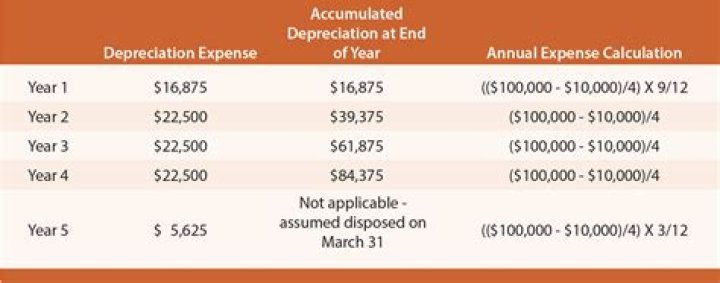

First, to establish account balances that are appropriate at the date of sale, depreciation is recorded for the period of use during the current year. Second, the amount received from the sale is recorded while the book value of the asset (both its cost and accumulated depreciation) is removed.

Is depreciation expense permanent or temporary?

Depreciation Expense is a temporary account since it is an income statement account. As a temporary account, Depreciation Expense will begin each accounting year with a zero balance and will have its balance at the end of the year closed to an equity account such as retained earnings or a proprietor’s capital account.

What is the accounting journal entry for depreciation?

The depreciation entry is an allocation of the asset’s cost, it is not an attempt to indicate the current market value of the asset.

When do you record depreciation as an expense?

When a fixed asset is acquired by a company, it is recorded at cost (generally, cost is equal to the purchase price of the asset). This cost is recognized as an asset and not expense. Depreciation expense is recorded to allocate costs to the periods in which an asset is used.

How is the depreciation of an equipment calculated?

The annual depreciation for the equipment as per the straight-line method can be calculated, Annual depreciation = $6,000 / 3 = $2,000 a year over the next 3 years. Therefore, it will be recorded according to the golden rule of accounting-

Are there any exceptions to the depreciation rule?

The one exception is a capital lease, where the company records it as an asset when acquired but pays for the asset over time, under the terms of the associated lease agreement. Finally, depreciation is not intended to reduce the cost of a fixed asset to its market value. Market value may be substantially different, and may even increase over time.