How do you record purchase of treasury stock?

To record a repurchase, simply record the entire amount of the purchase in the treasury stock account. Resale. If the treasury stock is resold at a later date, offset the sale price against the treasury stock account, and credit any sales exceeding the repurchase cost to the additional paid-in capital account.

Is purchasing treasury stock an asset?

Treasury Stock is a contra equity item. It is not reported as an asset; rather, it is subtracted from stockholders’ equity. The presence of treasury shares will cause a difference between the number of shares issued and the number of shares outstanding.

Why would a company buy its own shares of stock?

The effect of a buyback is to reduce the number of outstanding shares on the market, which increases the ownership stake of the stakeholders. A company might buyback shares because it believes the market has discounted its shares too steeply, to invest in itself, or to improve its financial ratios.

How do you account for retired treasury stock?

Under cost method, the journal entry for the retirement of treasury stock is made by debiting the common stock with par value of shares being retired, debiting additional paid-in capital (if any) associated with the shares being retired and crediting treasury stock with the cost of shares being retired.

How does the treasury stock journal entry work?

They are two methods of recording treasury stock: 1. Cost Method The cost method ignores the par value of the share of the company. Under the cost method, if the treasury stock is purchased, the following entry is passed with the actual amount of purchase. When these shares are sold at a later stage, the following entry is passed:

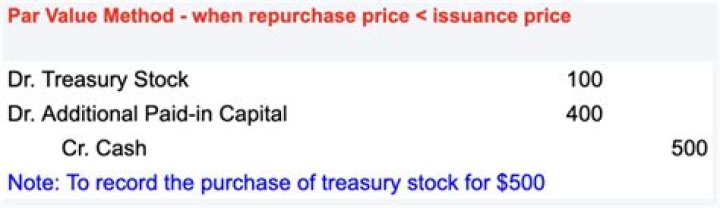

How is the purchase of treasury stock recorded?

Purchase of treasury stock – cost method: Journal entry: Under cost method, the treasury stock account is debited and cash account is credited with the amount paid for acquiring the shares of treasury stock (i.e., the cost of treasury stock). The par value of shares is ignored for recording the purchase of treasury stock under cost method.

How are reissuances credited to the treasury stock account?

They credit reissuances to the Treasury Stock account at the original cost of paid to reaquire the stock (not the par or stated value). Thus, the Treasury Stock account is debited at cost when shares are acquired and credited at cost when these shares are sold.

How does the treasury stock cost method work?

In this article we have explained the use of cost method, if you want to understand the use of par value method, read “ treasury stock – par value method ” article. Under cost method, the treasury stock account is debited and cash account is credited with the amount paid for acquiring the shares of treasury stock (i.e., the cost of treasury stock).