How does a typical variable life policy investment?

With a variable life insurance policy, you will be required to pay premiums into an account. The money in the account gets invested in a menu of investment options—typically mutual funds— that you can select. In addition, you may be able to allocate part of your premiums to a fixed account.

How does your money grow in life insurance?

When you make premium payments on a cash-value life insurance policy, one portion of the payment is allotted to the policy’s death benefit (based on your age, health, and other underwriting factors). As you continue to pay premiums on the policy and earn more interest, the cash value grows over the years.

What are the two components of a variable life insurance investment?

Every variable life insurance policy has three primary components: Death benefit. Cash value. Premium.

What is considered an element of a variable life policy?

How does variable life insurance work? There are three elements to variable life insurance, including a death benefit, cash value and premium. The premium is what you pay each month, some of which goes toward the cost of the insurance. The rest of the premium goes toward the investment accounts (sub-accounts).

How do I sell a variable life insurance policy?

Selling variable life insurance requires a state life insurance license, a series 6 license and a series 63 license. All states mandate these licenses, which allow holders to sell financial products that use or contain mutual funds and other variable-return securities.

How does a variable life insurance policy work?

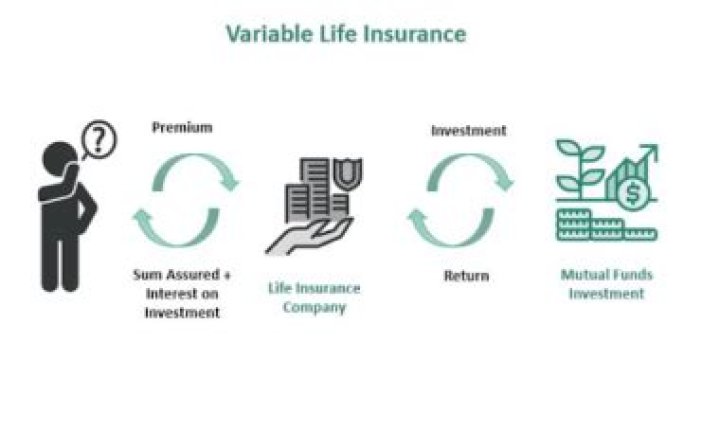

Variable life insurance is a permanent life insurance policy with an investment component. The policy has a cash-value account, which is invested in a number of sub-accounts available in the policy. A sub-account acts similar to a mutual fund, except it’s only available within a variable life insurance policy.

How does a variable universal life loan work?

VUL policies allow you to borrow money from the insurance company, using the policy’s cash value as collateral. Policy loans accrue interest (usually at a reasonable rate) but are not taxable as income. So, if structured properly, a VUL policy could be used as a tax-free deferred comp vehicle.

How does the cash value of a life insurance policy grow?

In the early years of your policy, a larger portion of your premium is invested and allocated to the cash value account. Generally, this cash value can grow quickly in the early years of the policy.

What happens if my variable universal life policy lapses?

That could be a massive tax bill if things don’t go well. The most common reason a VUL policy would lapse is if there’s not enough cash value left to pay policy expenses. Remember, this cash value is subject to volatile market performance just like any other investment.