How does arbitrage pricing theory differ from capital asset pricing method?

The APT serves as an alternative to the CAPM, and it uses fewer assumptions and may be harder to implement than the CAPM. While the CAPM formula requires the input of the expected market return, the APT formula uses an asset’s expected rate of return and the risk premium of multiple macroeconomic factors.

What common assumptions do the Capital Asset Pricing Model CAPM and arbitrage pricing theory APT share?

Assumptions of the Capital Asset Pricing Model That model assumes that all investors hold homogeneous expectations about mean return and variance of assets. It also assumes that the same efficient frontier is available to all investors.

What is included in arbitrage portfolio?

In the APT context, arbitrage consists of trading in two assets – with at least one being mispriced. The arbitrageur creates the portfolio by identifying n correctly priced assets (one per risk-factor, plus one) and then weighting the assets such that portfolio beta per factor is the same as for the mispriced asset.

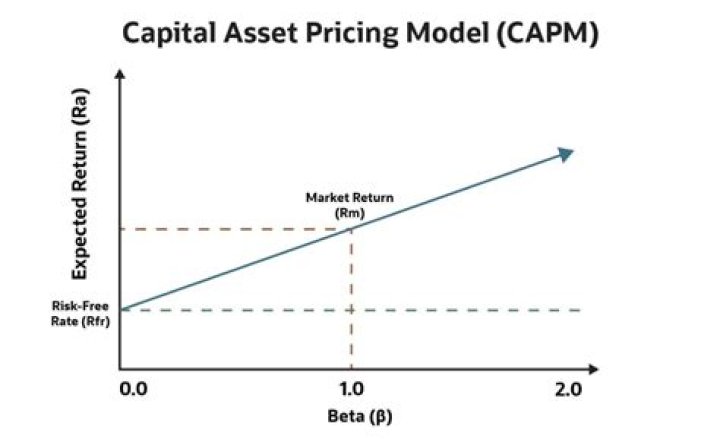

Is SML the same as CAPM?

The CAPM is a formula that yields expected return. SML is a graphical depiction of the CAPM and plots risks relative to expected returns. A security plotted above the security market line is considered undervalued and one that is below SML is overvalued.

What is the arbitrage theory of capital asset pricing?

Examines the arbitrage model of capital asset pricing as an alternative to the mean variance capital asset pricing model introduced by Sharpe, Lintner and Treynor.

Is the CAPM the same as the arbitrage pricing model?

There are inherent risks in holding any asset, and the capital asset pricing model (CAPM) and the arbitrage pricing model (APM) are both ways of calculating the cost of an asset and the rate of return which can be expected based on the risk level inherent in the asset (Krause, 2001).

What was the purpose of the arbitrage model?

The arbitrage model was proposed as an alternative to the mean variance capital asset pricing model, introduced by Sharpe, Lintner, and Treynor, that has become the major analytic tool for explaining phenomena observed in capital markets for risky assets.

Is there an opportunity for arbitrage in an asset portfolio?

Investors who are investing in the asset will be able to build the respective portfolios of their assets where there is an elimination of the risk with the help of diversification. There are some portfolios which are pretty well-diversified. There will be no opportunity for arbitrage on these portfolios.