How does LIFO vs FIFO affect net income?

LIFO and FIFO: Impact of Inflation In other words, the older inventory, which was cheaper, would be sold later. In an inflationary environment, the current COGS would be higher under LIFO because the new inventory would be more expensive. As a result, the company would record lower profits or net income for the period.

Why Net income is different for LIFO vs FIFO?

The main difference between LIFO and FIFO is based on the assertion that the most recent inventory purchased is usually the most expensive. If that assertion is accurate, using LIFO will result in a higher cost of goods sold and less profit, which also directly affects the amount of taxes you’ll have to pay.

Why does LIFO reduce net income?

LIFO is not a good indicator of ending inventory value because it may understate the value of inventory. LIFO results in lower net income (and taxes) because COGS is higher. However, there are fewer inventory write-downs under LIFO during inflation.

Why is LIFO banned?

IFRS prohibits LIFO due to potential distortions it may have on a company’s profitability and financial statements. For example, LIFO can understate a company’s earnings for the purposes of keeping taxable income low. It can also result in inventory valuations that are outdated and obsolete.

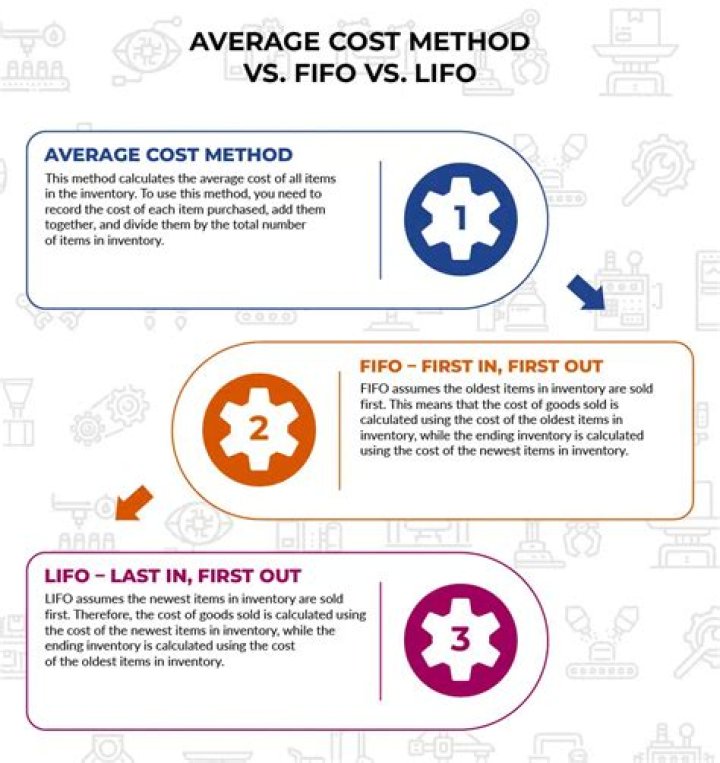

What is the cost flow method?

Cost flow assumptions refers to the method of moving the cost of a company’s product out of its inventory to its cost of goods sold. The cost of purchased goods with the intention of reselling. The cost of produced goods (including labor, material & manufacturing overhead costs)

What are the methods of cost flow assumptions?

In the U.S. the cost flow assumptions include FIFO, LIFO, and average. (If specific identification is used, there is no need to make an assumption.) FIFO, LIFO, average are assumptions because the flow of costs out of inventory does not have to match the way the items were physically removed from inventory.