How does the Sarbanes Oxley Act of 2002 impact the CEO CFO?

The Sarbanes-Oxley Act of 2002 requires the CEO and CFO of publicly traded companies to issue a statement certifying that the accompanying financial statements and disclosures fairly present, in all material respects, the operations and financial condition of the company.

What impact does implementing Sarbanes Oxley Act SOX have on corporate governance?

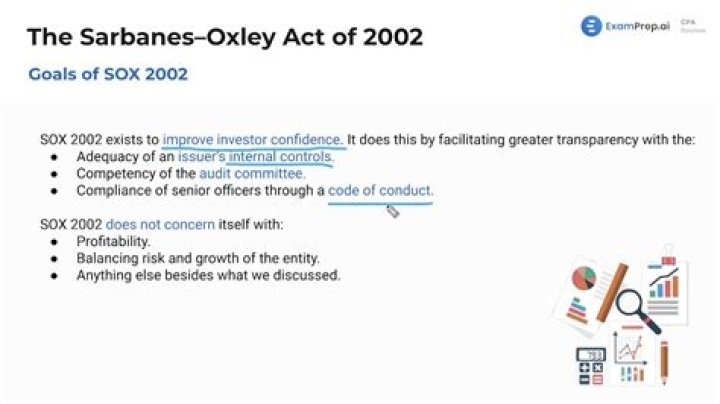

The act had a profound effect on corporate governance in the U.S. The Sarbanes-Oxley Act requires public companies to strengthen audit committees, perform internal controls tests, make directors and officers personally liable for the accuracy of financial statements, and strengthen disclosure.

How are CEOs and CFOs accountable under Section 404 of Sarbanes Oxley?

The CEO and CFO must certify that (a) the internal control system provides them with all material information, and (b) that they have evaluated the internal control system and found it (or they must identify the weaknesses). Section 404 requires an annual assessment of the Company’s —internal controls.

What are Sarbanes-Oxley Section 404 requirements?

SOX Section 404 (Sarbanes-Oxley Act Section 404) mandates that all publicly-traded companies must establish internal controls and procedures for financial reporting and must document, test and maintain those controls and procedures to ensure their effectiveness.

Is the Sarbanes-Oxley Act working?

But, lawyers and analysts say that for the most part Sarbanes-Oxley is working. It has strengthened auditing, made the accounting industry a better steward of financial standards, and fended off Enron-sized book-cooking disasters. Sarbanes-Oxley also increased criminal penalties for various kinds of financial fraud.

Which of the following is correct regarding internal controls?

The correct answer is letter “A”: An inherent limitation to internal control is the fact that controls can be circumvented by management override. Explanation: Internal controls limit fraud and other internal activities of the organizations.