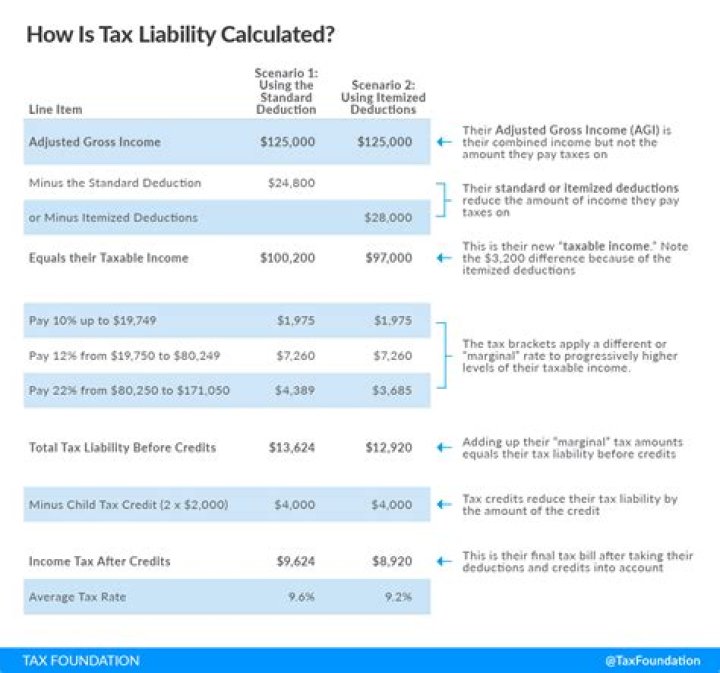

How is income tax calculated on house property?

Steps to compute “Income from House Property”

- a. Determining Gross Annual Value (GAV) of the property :

- b. Reduction of Municipal Taxes(property tax):

- c. Determination of Net Annual Value (NAV):

- d. Reduction of standard Deduction @30% of Net Annual Value:

- e. Reduction of home loan interest:

- f.

- g.

Which income is taxable under house property?

There is no income from your house property. Note: Since the gross annual value of a self-occupied house is zero, claiming the deduction on home loan interest will result in a loss from house property.

What is house property and its tax treatment in income tax?

In essence, any property such as house, building, office, warehouse is treated as ‘house property’ under the Income Tax Act. The ‘Income from House Property’ is one of the five heads of income that is taken into account for calculating the gross total income (GTI) of an assessee during the year.

Can income from house property be treated as business income?

v. Commissioner of Income Tax [2015] 373 ITR 673 (SC). Based on the above, the court, in the case of Rayala Corporation, ruled that income from house property received where the taxpayer is into the business of letting out property will be taxed as “Income from Business” and not as “Income from House Property”.

Which house property is not taxed?

Nothing is charged to tax under the head “Income from house property”. rule is applicable, even if the owner receives composite rent for both the lettings. In other words, in such a case, the composite rent is to be allocated for letting out of building and for letting of other assets.

Which property is always exempted from income tax?

Income from property confined to local authorities is tax-exempted as per Section 10(20). House property income of a political party is free from tax under Section 13A. Revenue earned from a property belonging to an approved scientific research association is exempted from tax under Section 10(21).

Is the rent from mobile antennae taxable as a house?

As long as the rent is for the space, terrace and roof space in this case and which space is certainly a part of the building, the rent can only be taxed as ‘income from house property’.

How much does it cost to lease a cell tower?

The average proposal for a new cell tower lease in our database for 2018-2019 was $1050/mo. Over the course of a standard 25-year lease, this would result in cumulative income to the landowner of $459,386.

What are the benefits of having a cell tower on your property?

Unlike commercial tenants or residential tenants, there is no maintenance burden (or very little) when it comes to cell tower tenants. They maintain their own lease area. They insure themselves. They pay for their own infrastructure and buildout. Transferable Asset. In most cases, the lease can be sold in the future.

Is the deduction for mobile antennae available under Section 24?

Issue – whether or not deduction under section 24 (a) @ 30% of the annual value is available in respect of computation of income under the head ‘income from house property’ in respect of income from renting of terrace for installation of mobile antenna. Facts : – Briefly stated, the relevant material facts of the case are as follow.