How is inventory accounted for when sold?

Inventory is recorded and reported on a company’s balance sheet at its cost. When an inventory item is sold, the item’s cost is removed from inventory and the cost is reported on the company’s income statement as the cost of goods sold. Cost of goods sold is likely the largest expense reported on the income statement.

When using a perpetual inventory system when is COGS calculated?

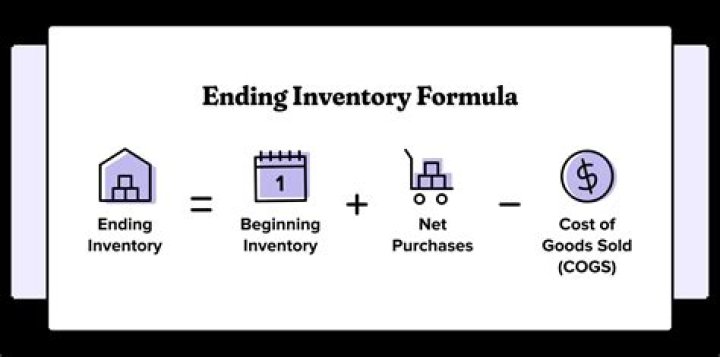

The cost of goods sold is calculated by adding the beginning inventory and purchases to obtain the cost of goods available for sale and then deducting the ending inventory.

How are purchases recorded in cost of goods sold?

Accumulate purchased inventory costs. As the accounting period progresses and the business receives invoices from suppliers for inventory items shipped to the company, record them either in a single purchases account or in whichever inventory asset account is most applicable.

How does the cost of goods sold journal entry work?

The cost of goods sold journal entry is: This entry matches the ending balance in the inventory account to the costed actual ending inventory, while eliminating the $450,000 balance in the purchases account. Advanced version: ABC International has a beginning balance in its inventory asset account of $1,000,000.

How are cost of goods sold and ending inventory calculated?

When perpetual methodology is utilized, the cost of goods sold and ending inventory are calculated at the time of each sale rather than at the end of the month. For example, in this case, when the first sale of 150 units is made, inventory will be removed and cost computed as of that date from the beginning inventory.

How does ABC record cost of goods sold?

It buys $350,000 of materials from suppliers during the month, which it records in the inventory account. At month-end, it counts its ending inventory and determines that there is $475,000 of inventory on hand. In addition, ABC incurs $150,000 of overhead costs, which it records in an overhead cost pool asset account.