How is inventory valued in QuickBooks?

QuickBooks uses the weighted average cost to determine the value of your inventory and the amount debited to COGS when you sell inventory. The average cost is the sum of the cost of all of the items in inventory divided by the number of items. You purchase a widget for $2.00.

Can you use QuickBooks for inventory?

QuickBooks Online has everything you need to manage your inventory. Inventory features are available for QuickBooks Online Plus and Advanced. If you don’t have Plus or Advanced, upgrade your QuickBooks plan to start tracking your inventory.

How do you adjust inventory value in QuickBooks?

To adjust inventory in QuickBooks Desktop Pro, select “Vendors| Inventory Activities| Adjust Quantity/Value on Hand” from the Menu Bar to open the “Adjust Quantity/Value on Hand” window. Select the type of inventory adjustment to make from the “Adjustment Type” drop-down menu.

How do I enter inventory quantity in QuickBooks?

To do that:

- Select on + New.

- Under Other, choose on Inventory Qty Adjustment.

- Enter the Adjustment Date.

- In the Inventory adjustment account drop-down, select the COGS account.

- Select the products in the Product field drop-down.

- For each item, enter either a new quantity or a change in quantity.

- Select Save and close.

How to adjust your inventory quantity or value in QuickBooks?

Select the Adjustment Type ▼ drop-down, then select Quantity, Total Value, or Quantity and Total Value. Select the adjustment type option and then select your adjustment account. Enter the Adjustment Date. Select the Adjust Account ▼ drop-down, then select the adjustment account you set up. Add Reference No.

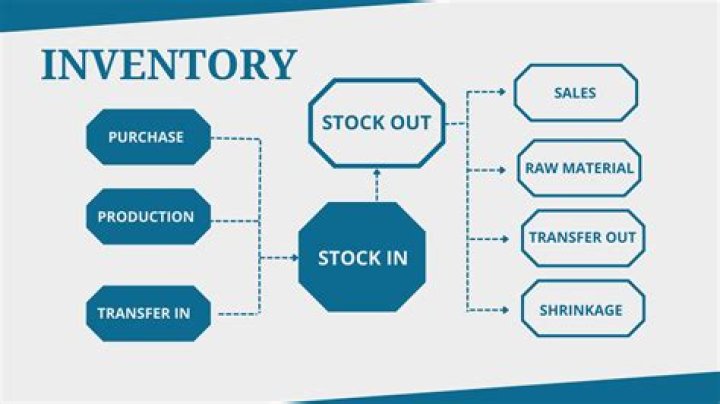

How are items recorded in inventory in QuickBooks?

As the items are purchased, they are recorded on the items tab of a bill, check or credit card charge) and the inventory balance is increased for the quantity and cost of the item. When the item is sold, the average cost is deducted from the inventory asset account and recorded in cost of goods sold.

Do you have to pay taxes on inventory in QuickBooks?

You don’t want to have to pay taxes on inventory that you don’t have; therefore, you should always take a regular count and adjust your records as necessary. With QuickBooks, it is a very simple process to make these adjustments. Select “Lists” or “Vendors. ” Select “Items” under Lists or “Inventory Activities” under Vendors.

How is non-inventory reported on a QuickBooks balance sheet?

Clients often set up items as type – inventory, when they would be better served using the non-inventory item type. The non-inventory type does not keep a perpetual count or an average cost. Second, evaluate whether the total inventory value on the inventory valuation summary report agrees to the inventory amount reported on the Balance Sheet.