How is the MACRS deduction calculated in the year of disposition for an asset that has been depreciated using the half year convention?

Transcribed image text: How is the MACRS deduction calculated in the year of disposition for an asset that has been depreciated using the half- year convention? The total depreciation allowed for the year is: O Multiplied by 1/2 O Divided by 1/2 O Multiplied by 1/4.

Can I write off a computer for my small business?

Computers you purchase to use in your business or on the job are a deductible business expense. If fact, you may be able to deduct the entire cost in a single year.

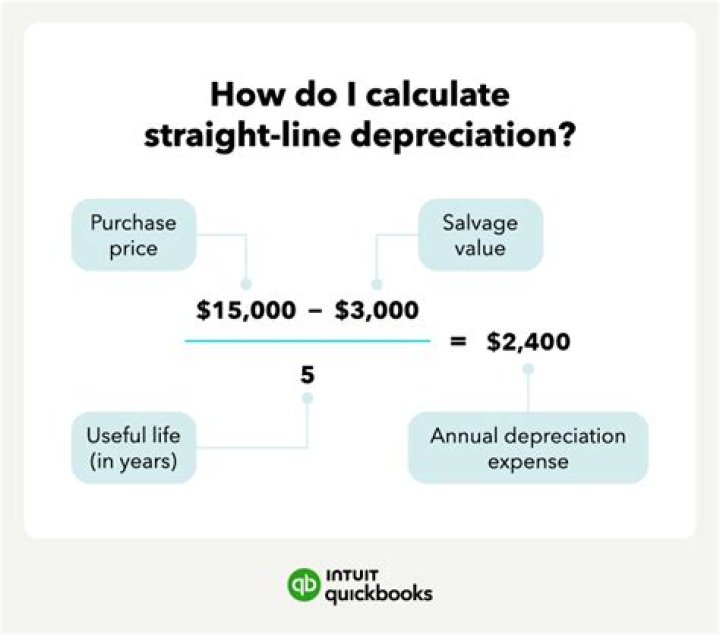

Why is MACRS better than straight-line?

MACRS allows for greater accelerated depreciation over longer time periods. This is beneficial since faster acceleration allows individuals and businesses to deduct greater amounts during the first few years of an asset’s life, and relatively less later.

Where does the MACRS asset life table come from?

The MACRS Asset Life table is derived from Revenue Procedure 87-56 1987-2 CB 674. The table specifies asset lives for property subject to depreciation under the general depreciation system provided in section 168 (a) of the IRC or the alternative depreciation system provided in section 168 (g).

What’s the recovery period for a MAcr property?

Property described in asset class 00.12 which is qualified technological equipment as defined in section 168(i)(2) is assigned a recovery period of 5 years notwithstanding its class life. 00.13 Data Handling Equipment, Except Computers

What do you need to know about MACRS depreciation?

To calculate depreciation using MACRS, you’ll need the following info: The depreciation system you need to use – GDS or ADS. The property classification of your asset. The cost basis of the asset. The convention. The depreciation method.

How many classifications are there for MACRS GDS and ads?

There are nine property classifications for MACRS GDS and ADS. Below is a summary table of 3, 5, and 7 year property classes. You can find the full list in IRS Pub 946. The cost basis for an asset is any costs incurred so that you can start using it in your business.